Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Life-Changing Events That Move the Housing Market

Life is a journey filled with unexpected twists and turns, like the excitement of welcoming a new addition, retiring and starting a new adventure, or the bittersweet feeling of an empty nest. If something like this is changing in your own life, you may be considering buying or selling a house. That’s because through all these life-altering events, there is one common thread—the need to move.

Reasons People Still Need To Move Today

According to the National Association of Realtors (NAR) there have been a lot of this type of milestone or life change over the last two years (see graph below):

And, these big life changes are going to continue to impact people moving forward, even with the current affordability challenges brought on by higher mortgage rates and rising home prices.

As Claire Trapasso, Executive News Editor at Realtor.com, says:

“Because high mortgage rates, elevated home prices, and stubbornly low inventory make today’s housing market particularly challenging, many of today’s buyers are motivated by life changes, such as growing families, supporting elderly parents or grown children, or accommodating professional needs. . .”

Lean On a Real Estate Professional for Help

Whether you’re beginning your search for a home or preparing to sell your current house, you don’t have to go it alone. With their expertise, a real estate agent is an invaluable partner who can help you smoothly transition through these big moments in your life. Here are just a few examples.

When Buying a Home

If you’re welcoming a new addition and want more space, the need for a new home may be a top priority. While higher home prices and mortgage rates are creating challenges for buyers, you may have to find a way to meet your changing needs, even with today’s mortgage rates.

A skilled real estate agent can help. Their expertise and knowledge of the local housing market can save you a considerable amount of time and stress. An agent will take the time to understand your specific needs, budget, and preferences, allowing them to narrow down your search and present you with suitable options.

When Selling a House

If you’re retiring or going through a separation or divorce, your main focus may be to make the most out of your investment when selling your house, so you can find one that works better for you moving forward.

This is another place where a real estate agent’s expertise truly shines. They can accurately assess your home’s market value, suggest improvements to enhance its appeal, and craft a strategic marketing plan. Their negotiation skills are a big asset when it comes to making sure you get a fair price for your house, allowing you to move on to the next chapter of your life with confidence and peace of mind.

No matter your situation, lean on a trusted professional for help as you buy or sell a home.

Bottom Line

If recent life-changing events have you wanting or needing to move, let’s connect.

How VA Loans Can Help Make Homeownership Dreams Come True

For more than 79 years, Veterans Affairs (VA) home loans have helped millions of veterans buy their own homes. If you or someone you care about has served in the military, it’s essential to learn about this program and its advantages.

Here are some important things to know about VA loans before you buy a home.

The Many Advantages of VA Home Loans

VA home loans provide a pathway to homeownership for those who have served our nation, and they’re a great benefit for buyers who qualify. According to the Department of Veteran Affairs:

- Options for No Down Payment: Qualified borrowers can often purchase a home with no down payment. That’s a huge weight lifted when you’re trying to save for a home.

- Limited Closing Costs: There are limits on the types of closing costs you pay when you qualify for a VA home loan. So, more money stays in your pocket when it’s time to seal the deal.

- Don’t Require Private Mortgage Insurance (PMI): Many other loans with down payments under 20% require PMI. VA loans do not, which means veterans can save on their monthly housing costs.

A recent article from Veterans United sums up just how impactful this loan option can be:

“For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.”

Bottom Line

Owning a home is the American Dream. Veterans sacrifice a lot to protect our country, and one way we can show our appreciation is by making sure they know all the benefits of VA home loans. Thank you for your service.

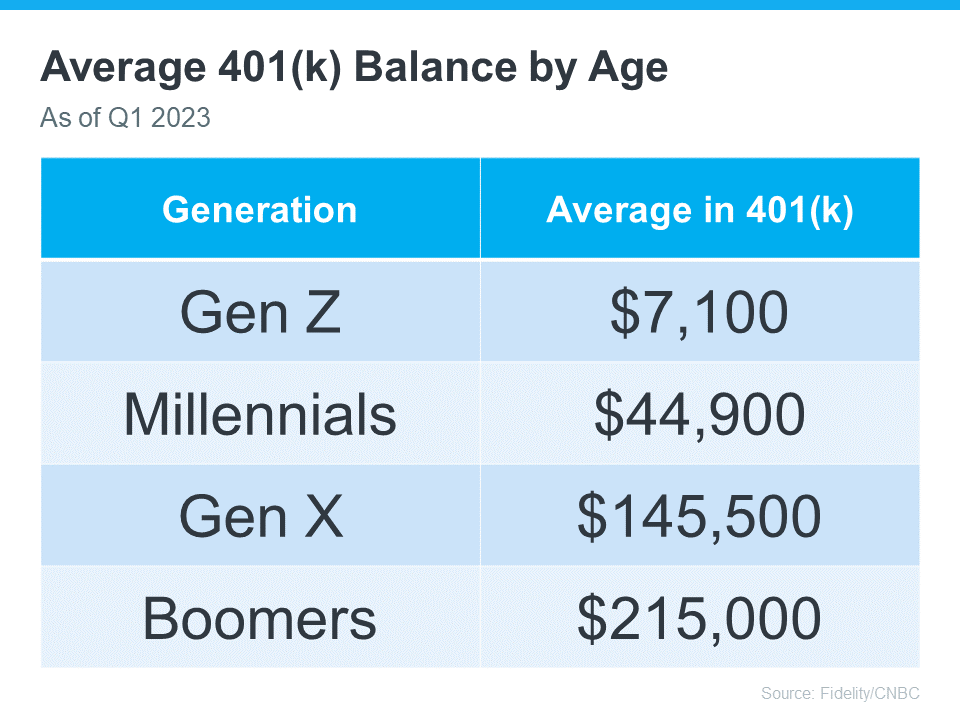

Thinking About Using Your 401(k) To Buy a Home?

Are you dreaming of buying your own home and wondering about how you’ll save for a down payment? You’re not alone. Some people think about tapping into their 401(k) savings to make it happen. But before you decide to dip into your retirement to buy a home, be sure to consider all possible alternatives and talk with a financial expert. Here’s why.

The Numbers May Make It Tempting

The data shows many Americans have saved a considerable amount for retirement (see chart below):

It can be really tempting when you have a lot of money saved up in your 401(k) and you see your dream home on the horizon. But remember, dipping into your retirement savings for a home could cost you a penalty and affect your finances later on. That’s why it’s important to explore all your options when it comes to saving for a down payment and buying a home. As Experian says:

“It’s possible to use funds from your 401(k) to buy a house, but whether you should depends on several factors, including taxes and penalties, how much you’ve already saved and your unique financial circumstances.”

Alternative Ways To Buy a Home

Using your 401(k) is one way to finance a home, but it’s not the only option. Before you decide, consider a couple of other methods, courtesy of Experian:

- FHA Loan: FHA loans allow qualified buyers to put down as little as 3.5% of the home’s price, depending on their credit scores.

- Down Payment Assistance Programs: There are many national and local programs that can help first-time and repeat homebuyers come up with the necessary down payment.

Above All Else, Have a Plan

No matter what route you take to purchase a home, be sure to talk with a financial expert before you do anything. Working with a team of experts to develop a concrete plan prior to starting your journey to homeownership is the key to success. Kelly Palmer, Founder of The Wealthy Parent, says:

“I have seen parents pausing contributions to their retirement plans in favor of affording a larger home often with the hope they can refinance in the future… As long as there is a tangible plan in place to get back to saving for their retirement goals, I encourage families to consider all their options.”

Bottom Line

If you’re still thinking about using your 401(k)-retirement savings for a home down payment, consider all your options and work with a financial professional before you make any decisions.

The Benefits of Buying a Multi-Generational Home

Some Highlights

- If you’re ready to buy a home but are having a hard time affording it on your own, or, if you have aging loved ones you need to care for, you might want to consider a multi-generational home.

- Living with siblings, parents, and even grandparents can help you save money, give or receive childcare, and spend quality time together.

- Let’s connect to find a home in our area that’s perfect for you and your loved one’s needs.

What Are Accessory Dwelling Units and How Can They Benefit You?

Maybe you’re in the market for a home and are having a hard time finding the right one that fits your budget. Or perhaps you’re already a homeowner in need of extra income or a place for loved ones. Whether as a potential homebuyer or a homeowner with changing needs, accessory dwelling units, or ADUs for short, may be able to help you reach your goals.

What Is an ADU?

As AARP says:

“An ADU is a small residence that shares a single-family lot with a larger, primary dwelling.”

“An ADU is an independent, self-contained living space with a kitchen or kitchenette, bathroom and sleeping area.”

“An ADU can be located within, attached to, or detached from the main residence. It can be created out of an existing structure (such as a garage) or built anew.”

If you’re thinking about whether an ADU makes sense for you as a buyer or a homeowner, here’s some useful information and benefits that ADUs can provide. Keep in mind, that regulations for ADUs vary based on where you live, so lean on a local real estate professional for more information.

The Benefits of ADUs

Freddie Mac and the AARP identify some of the best features of ADUs for both buyers and homeowners:

- Living Close by, But Still Separate: ADUs allow loved ones to live together while having separate spaces. That means you can enjoy each other’s company and help each other out with things like childcare, but also have privacy when needed. If this appeals to you, you may want to consider buying a home with an ADU or adding an ADU onto your house. According to Freddie Mac:

“Having an accessory dwelling unit on an existing property has become a popular way for homeowners to offer independent living space to family members.”

- Aging in Place: Similarly, ADUs allow older people to be close to loved ones who can help them if they need it as they age. It gives them the best of both worlds – independence and support from loved ones. For example, if your parents are getting older and you want them nearby, you may want to buy a home with an ADU or build one onto your existing house.

- Affordable To Build: Since ADUs are often on the smaller side, they’re typically less expensive to build than larger, standalone homes. Building one can also increase your property’s value.

- Generating Additional Income: If you own a home with an ADU or if you build an ADU on your land, it can help generate rental income you could use toward your own mortgage payments. It’s worth noting that because an ADU exists on a single-family lot as a secondary dwelling, it typically cannot be sold separately from the primary residence. But that’s changing in some states. Work with a professional to understand your options.

These are a few of the reasons why many people who benefit from ADUs think they’re a good idea. As Scott Wild, SVP of Consulting at John Burns Research, says:

“It’s gone from a small niche in the market to really a much more impactful part of new housing.”

Bottom Line

ADUs have some great advantages for buyers and homeowners alike. If you’re interested, reach out to a real estate professional who can help you understand local codes and regulations for this type of housing and what’s available in your market.

Foreclosures and Bankruptcies Won’t Crash the Housing Market

If you’ve been following the news recently, you might have seen articles about an increase in foreclosures and bankruptcies. That could be making you feel uneasy, especially if you’re thinking about buying or selling a house.

But the truth is, even though the numbers are going up, the data shows the housing market isn’t headed for a crisis.

Foreclosure Activity Rising, but Less Than Headlines Suggest

In recent years, the number of foreclosures has been very low. That’s because, in 2020 and 2021, the forbearance program and other relief options were put in place to help many homeowners stay in their homes during that tough time.

When the moratorium ended, there was an expected rise in foreclosures. But just because they’re up, that doesn’t mean the housing market is in trouble.

To help you see how much things have changed since the housing crash in 2008, check out the graph below using research from ATTOM, a property data provider. It looks at properties with a foreclosure filing going all the way back to 2005 to show that there have been fewer foreclosures since the crash.

As you can see, foreclosure filings are inching back up to pre-pandemic numbers, but they’re still way lower than when the housing market crashed in 2008. And today, the tremendous amount of equity American homeowners have in their homes can help people sell and avoid foreclosure.

The Increase in Bankruptcies Isn’t Dramatic Either

As you can see below, the financial trouble many industries and small businesses felt during the pandemic didn’t cause a dramatic increase in bankruptcies. Still, the number of bankruptcies has gone up slightly since last year, nearly returning to 2021 levels. But that isn’t cause for alarm.

The numbers for 2021 and 2022 were lower than more typical years. That’s in part because the government provided trillions of dollars in aid to individuals and businesses during the pandemic. So, let’s instead focus on the bar for this year and compare it to the bar on the far left (2019). It shows the number of bankruptcies today is still nowhere near where it was before the pandemic. Both of these two factors are reasons why the housing market isn’t in danger of crashing.

Bottom Line

Right now, it’s crucial to understand the data. Foreclosures and bankruptcies are rising, but these leading indicators aren’t signaling trouble that would cause another crash.

A Real Estate Agent Helps Take the Fear Out of the Market

Do negative headlines and talk on social media have you feeling worried about the housing market? Maybe you’ve even seen or heard something lately that scares you and makes you wonder if you should still buy or sell a home right now.

Regrettably, when news in the media isn’t easy to understand, it can make people feel scared and unsure. Similarly, negative talk on social media spreads fast and creates fear. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You should lean on a trusted real estate agent to help you separate fact from fiction and get the answers you need.

That agent will use their knowledge of what’s really happening with home prices, housing supply, expert forecasts, and more to give you the best possible advice. The National Association of Realtors (NAR) explains:

“. . . agents combat uncertainty and fear with a combination of historical perspective, training and facts.”

The right agent will help you figure out what’s going on at the national level and in your local area.

They’ll debunk headlines using data you can trust. Plus, they have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

Bottom Line

If you need reliable information about the housing market and expert advice about your own move, let’s connect.

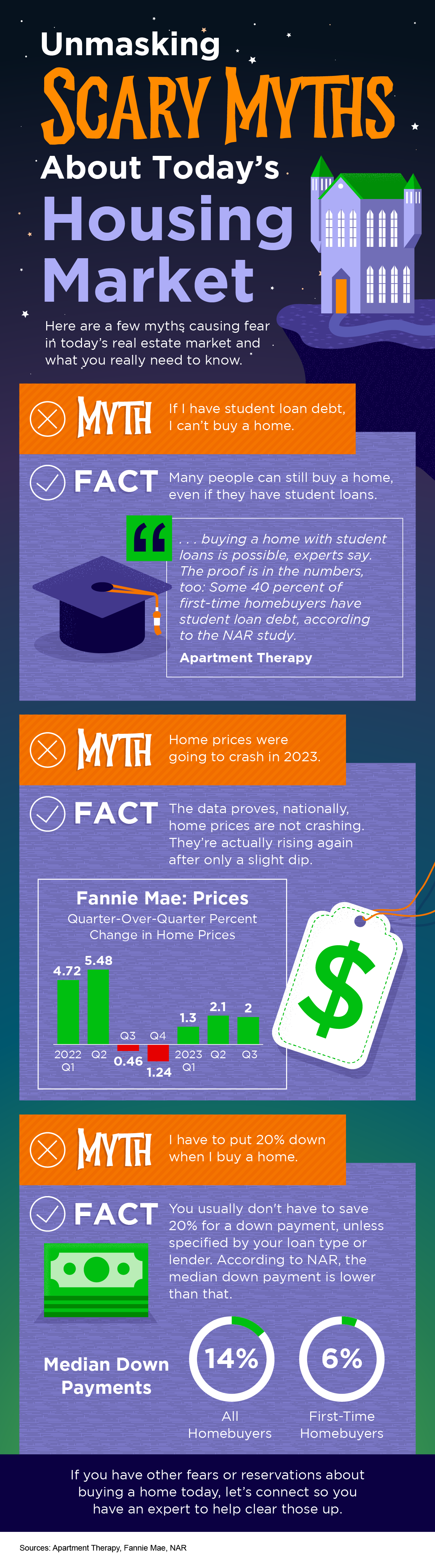

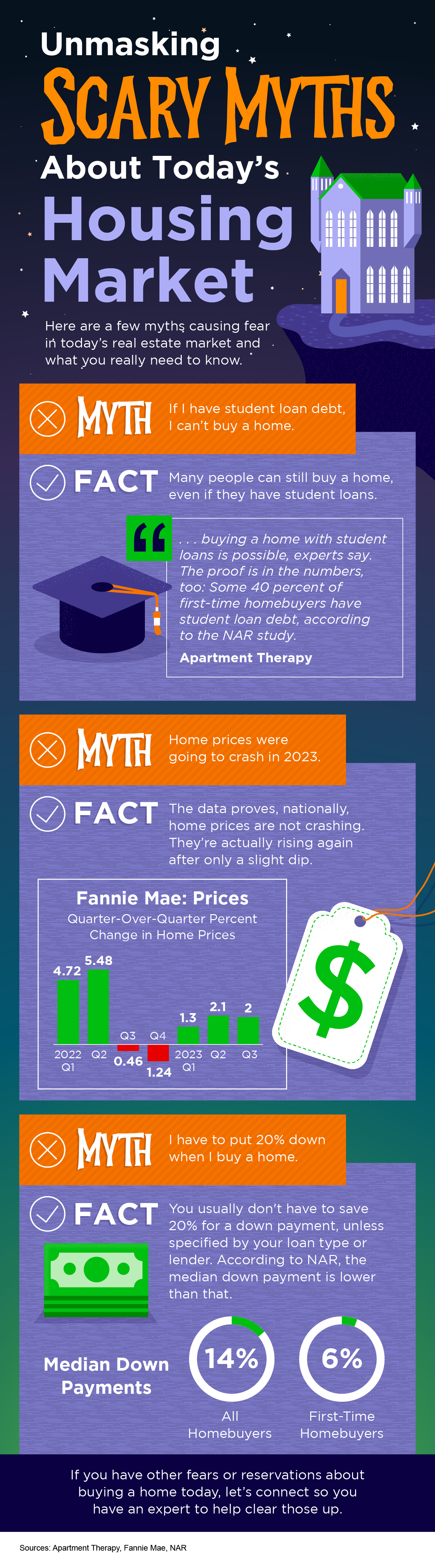

Unmasking Scary Myths about Today’s Housing Market

Some Highlights

- Here’s what you really need to know about a few myths causing fear in today’s housing market.

- Despite common misconceptions, many people can buy a home even if they have student loans, home prices are rising nationally (not falling), and you usually don’t have to have 20% for a down payment.

- If you have other fears or reservations about buying a home today, let’s connect so you have an expert to help clear those up.

Affordable Homeownership Strategies for Gen Z

The idea of owning a home has always been a big part of the American Dream. It’s a symbol of stability, independence, and having a place to truly call your own. But for Gen Z, the “Zoomers” born between 1997 and 2012, making that dream a reality can feel like quite the challenge today with higher mortgage rates and rising home prices.

But achieving that goal of owning your first home can still be attainable, even today, with some strategic planning and resourcefulness.

Explore Down Payment Assistance Options

With prices rising all around you, it can be hard to save up for a home. If you’ve been struggling to stash away enough cash for that down payment, it’s worth it to look into the various down payment assistance programs available. These programs can really help you save big on the upfront costs of buying a home.

There are a lot more options out there than you may realize. According to Down Payment Resource, there are over 2,000 programs designed to help hopeful homebuyers with down payments and closing costs.

If you qualify for one of these programs, you may not need to save up as much money for your down payment. A local real estate agent can help you explore these programs in your area, making it much easier to turn your homeownership dream into a reality.

Consider Living with Relatives To Save

If you still need a bit more time to save, even with the down payment assistance programs out there, there are ways you can make that happen. Many savvy Zoomers have made a strategic choice to live with relatives so they can get to their savings goals even faster.

According to the National Association of Realtors (NAR), around 30% of Gen Z homebuyers transition directly from their relative’s home to a home of their own.

By sharing living costs, such as mortgage payments, utility bills, and even grocery expenses, you can substantially reduce your monthly expenses. This frees up more of your income to tackle any outstanding debt, boost your credit score, and reach your down payment target in less time. And, all of this can bring homeownership one step closer to becoming a reality. Clare Trapasso, Executive News Editor at Realtor.com, explains:

“Faced with ongoing housing affordability issues . . . we’re seeing parents and children becoming roommates again in later years as the ‘kids’ save up to purchase their own place . . .”

The Road to Homeownership

When you’re on the path to becoming a homeowner, it’s a good idea to get some help along the way. And one of your best resources on this journey as a young homebuyer is a trusted real estate agent. They’ll steer you through the process of buying a home and help you find one you can afford.

Bottom Line

For Gen Z, the path to homeownership may not be straightforward, but it’s still within reach. With the right strategies, you can turn your dream of owning a home into a reality.

Invest in Yourself by Owning a Home

Are you wondering if it makes sense to buy a home right now? While today’s mortgage rates might seem a bit intimidating, here are two compelling reasons why it still may be a good time to become a homeowner.

Home Values Appreciate over Time

There’s been a lot of confusion around what’s happened with home prices over the past two years. While they did dip ever so slightly in late 2022, this year they’ve been appreciating at a more normal pace, which is good news for the housing market. And while looking at price movement over just a year or two can make you worry prices are usually this unpredictable, history shows in the long run, home values rise (see graph below):

Using data from the Federal Reserve for the past 60 years, you can see the overall trend is home prices have climbed quite steadily. Sure, there was an exception around the housing crash of 2008 that caused prices to break the usual trend for a time, but overall, home values have been consistently on the rise.

Increasing home values is one great reason why buying may make more sense than renting. As prices rise, and as you pay down your mortgage, you build equity. Over time, that growing equity gives your net worth a boost.

Rent Keeps Going Up Through the Years

Another reason you may want to consider buying a home instead of renting is the never-ending rent hike. If you’ve ever felt the pinch of rent increasing year after year, you’re not alone. That’s because, rents have climbed steadily over the past six decades (see graph below):

By buying a home, you can lock in your monthly housing costs and bid farewell to those pesky rent hikes. That stability is a game-changer.

In the end, it all boils down to this: your housing payments are an investment, and you’ve got a choice to make. Do you want to invest in yourself or your landlord?

By becoming a homeowner, you’re investing in your own future. When you rent, that’s money you never get back.

When you factor in home values consistently rising, plus the opportunity to get relief from never-ending rent hikes, homeownership can be a path to financial security. As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), states:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line

When it comes down to it, buying a home offers more benefits than renting, even when mortgage rates are high. If you want to avoid increasing rents and take advantage of long-term home price appreciation, let’s connect to go over your options.