Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

A shift is underway in the housing market this season. And if you’ve been sitting on the sidelines waiting for the right moment to jump back into your homebuying search, this is a great time to do it. That’s because the best week to buy a home this year is just around the corner. Your sweet spot is here.

The experts at Realtor.com study seasonal trends to figure out the ideal week for homebuyers:

“Nationally, the best time to buy in 2024 is the week of Sept. 29–Oct. 5. This week historically has shown the best balance of market conditions that favor buyers. Inventory tends to be high, prices are below peak levels, demand is waning, and the pace of the market slows to a more manageable speed.”

In addition to the historical trends and typical seasonality that Realtor.com looks at, there are also clear indicators in today’s market data that you’ll see better conditions right now than you would have over the last few years.

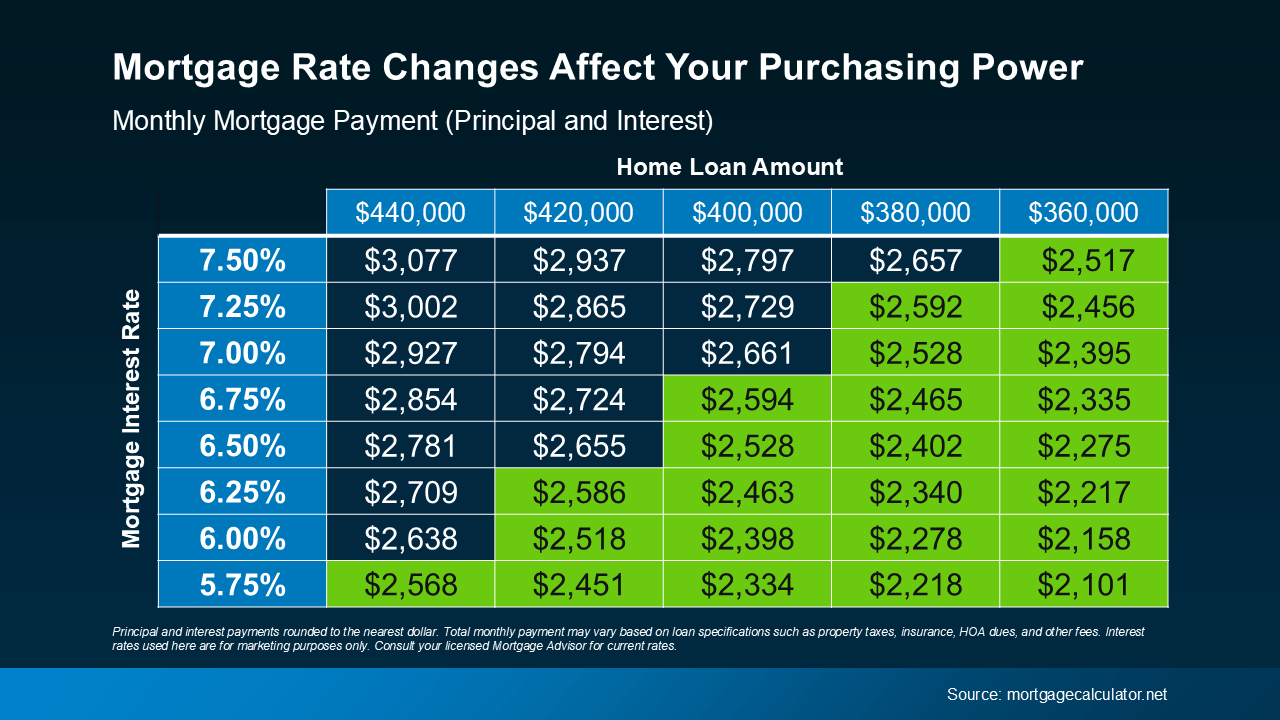

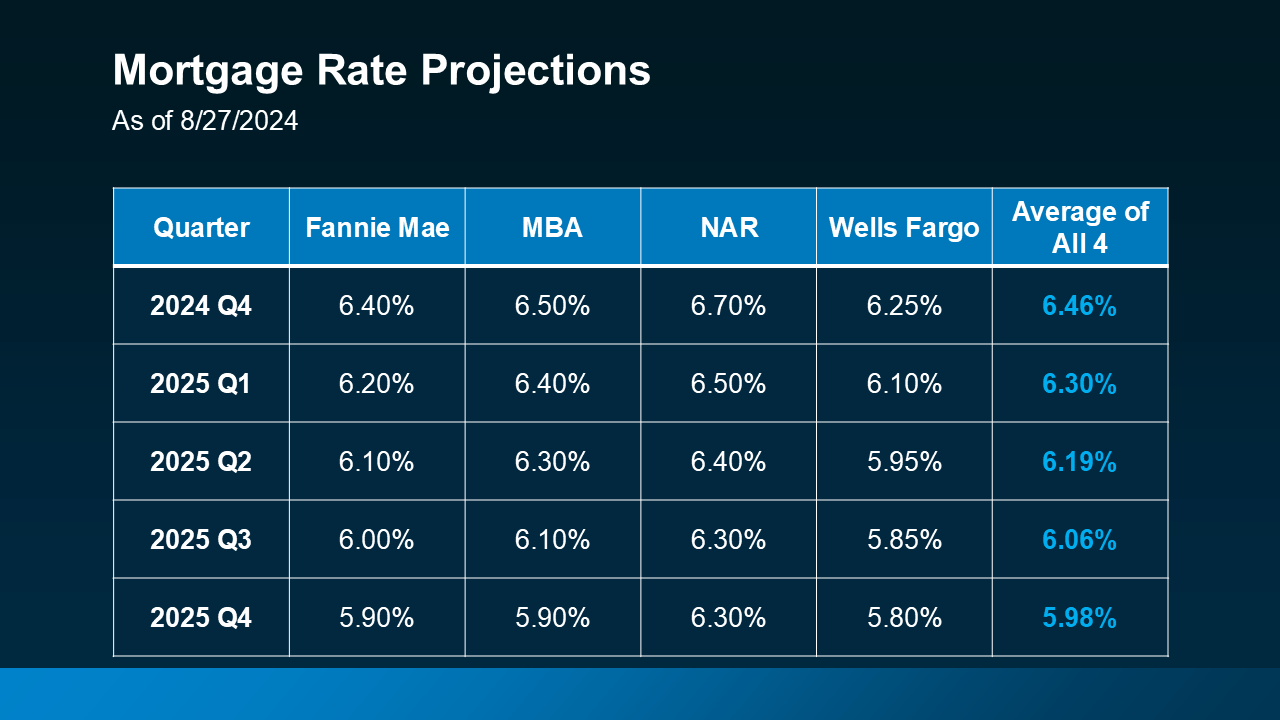

Mortgage rates just hit their lowest point in 19 months, and that goes a long way to help with your purchasing power and affordability. Andy Walden with Intercontinental Exchange Inc. (ICE) points out:

“Recent easing in mortgage rates brought some much-sought relief to prospective homebuyers. Along with a general cooling in home price growth, rates falling below 6.5 percent made August the most affordable month for housing since February.”

And Ralph McLaughlin, Senior Economist at Realtor.com, explains that it’s not just rates that have improved – inventory has too:

“The number of homes actively for sale continues to be elevated compared with last year, growing by 35.8%, a 10th straight month of growth, and now sits at the highest since May 2020.”

That should give you more options. At the same time, sellers now have to compete with each other for your attention. That means they’ll be more likely to negotiate because they know their house will sit on the market longer if they don’t. As Zillow says:

“Buyers waiting on the sidelines could find that early fall presents a ‘sweet spot,’ where there’s less competition from other buyers, more motivated sellers and lower interest rates to finance their purchases.”

Bottom Line

If you want to make sure you’re ready to take advantage of this sweet spot, let’s connect and start the prep work now. Maybe it’s time to get off the sidelines and into the action.

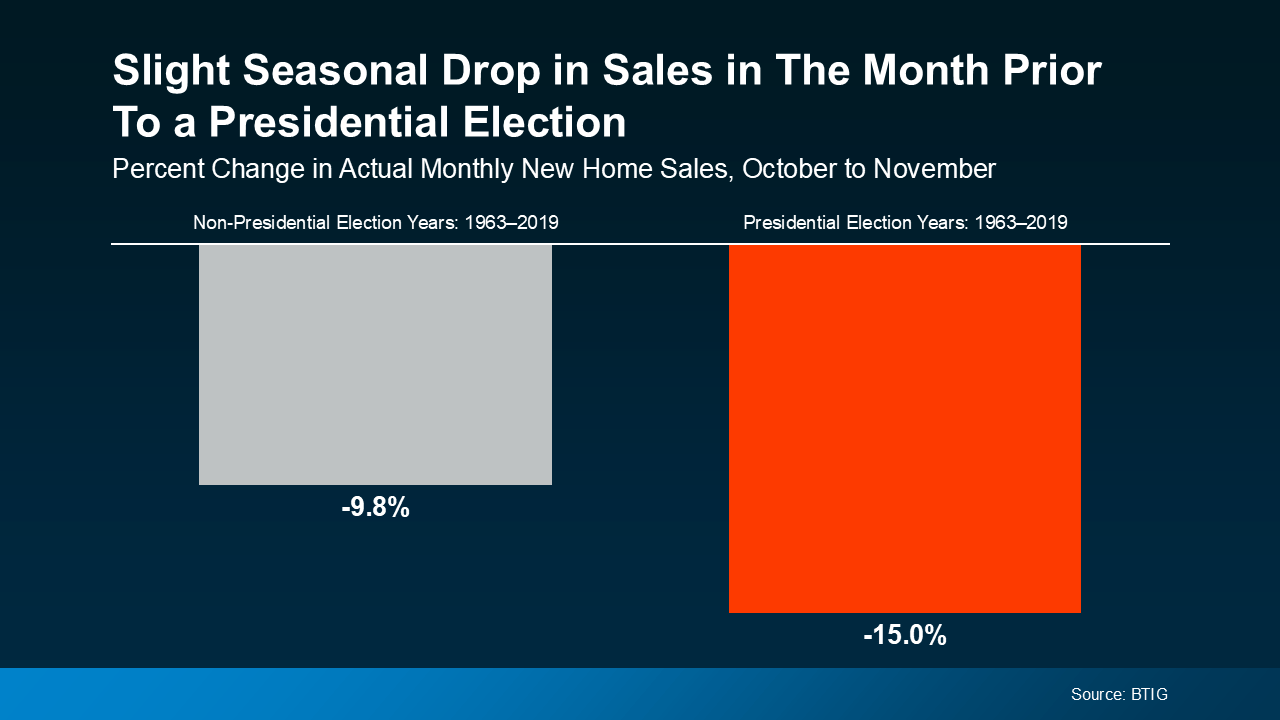

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary.

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary. Home Prices

Home Prices