Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

When your house doesn’t sell, it’s not just disappointing. It messes with your timing. Your plans. Your confidence. You start second-guessing everything, including the decision to move in the first place. And that raises 2 big questions:

Do you try again?

Is that even worth it?

Here’s the secret to getting a better outcome the second time around.

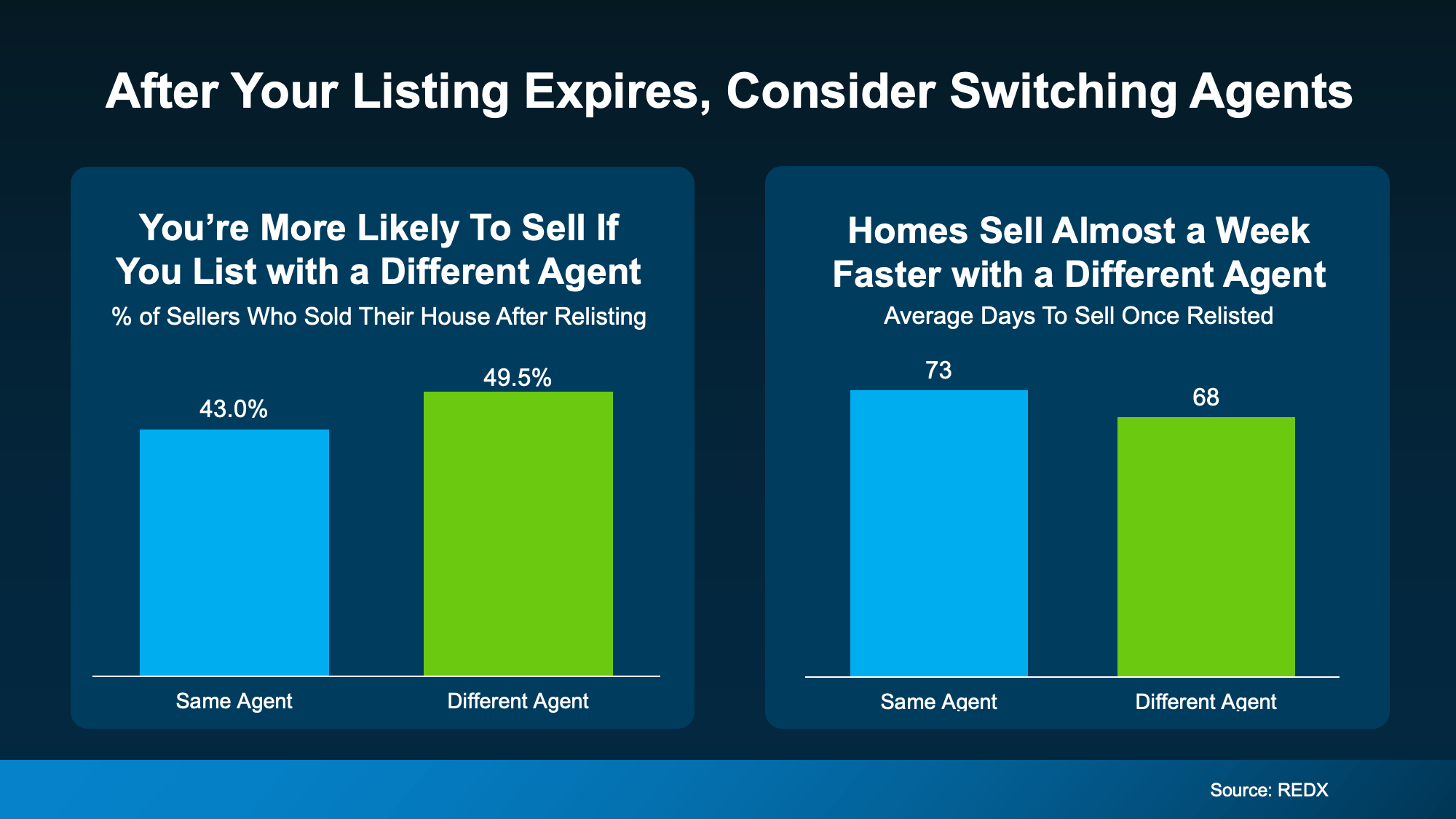

Different Agent. Different Results.

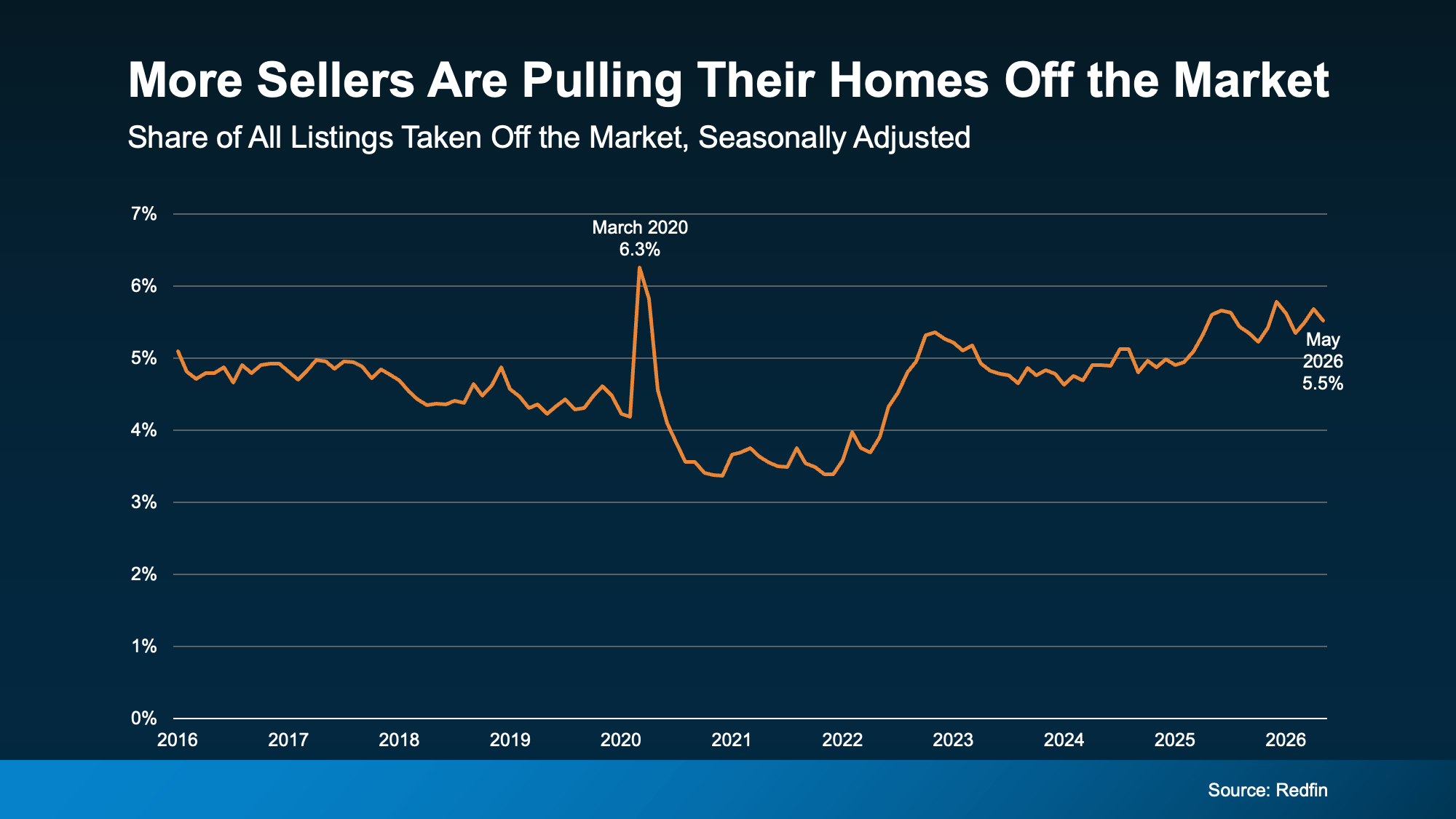

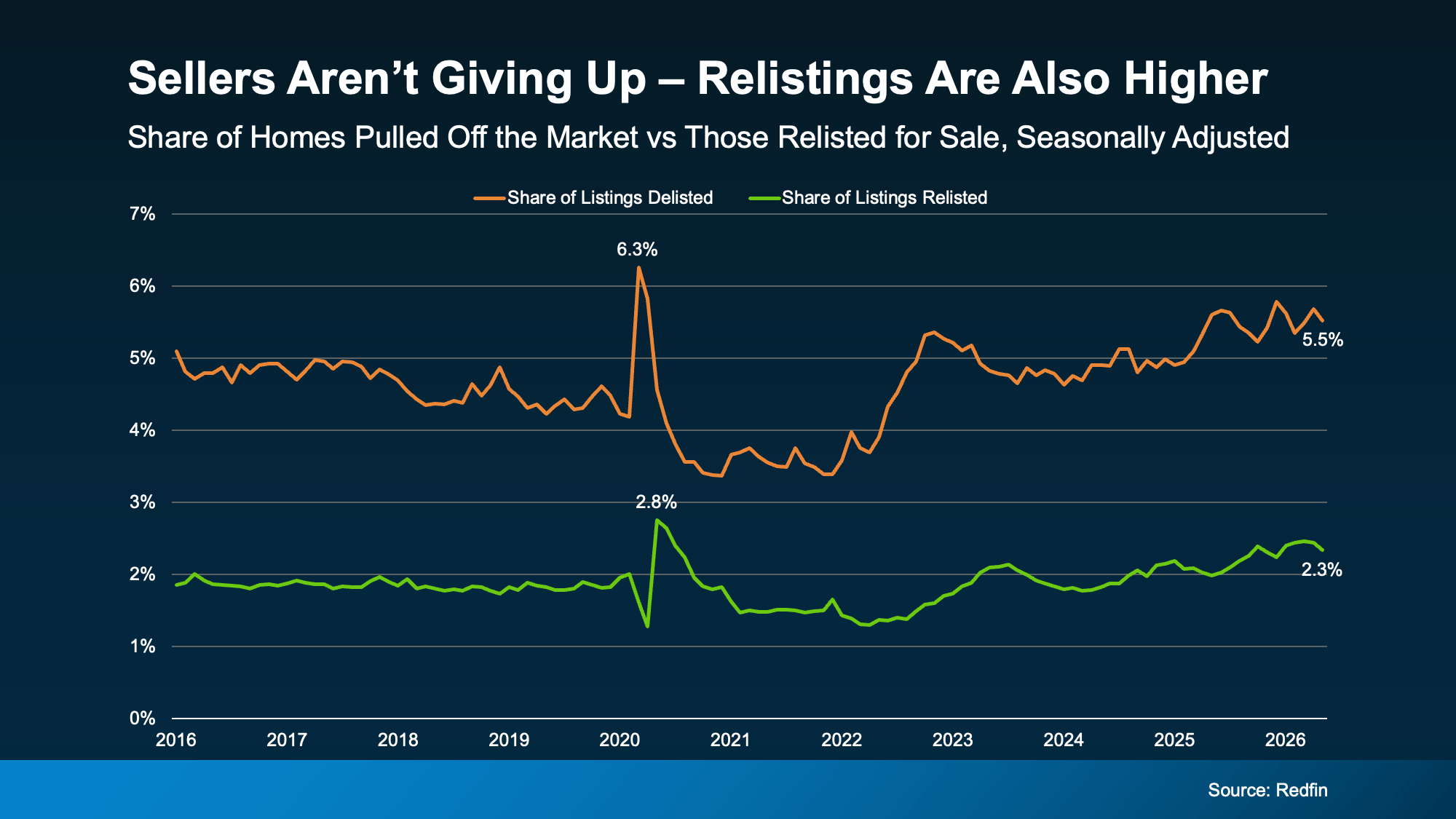

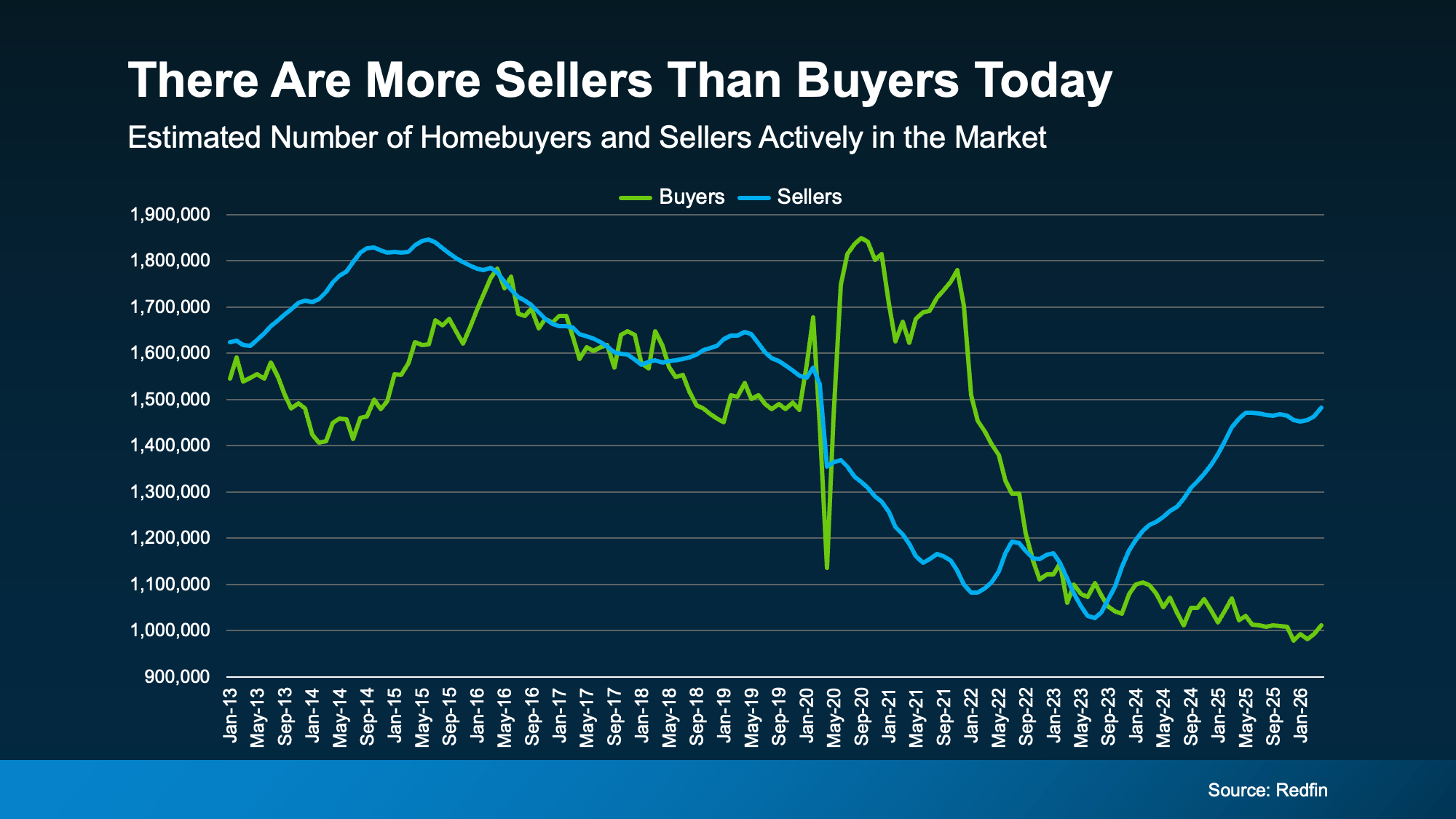

Most sellers who re-list and ultimately sell don’t wait for market to magically change. They change their approach. And there’s data to back that up.

Research from REDX shows homeowners who put their house back on the market with a different agent are more likely to sell than homeowners who re-used the same agent. Not to mention, they see their homes sell faster (see graph below):

That’s the power of a fresh set of eyes. Because in a moment like this, the worst thing you can do is rerun the same set of plays and expect a different outcome. A different agent can bring a new perspective on where things went off track – and a lot of the time, one of these things happened.

1. The Asking Price Didn’t Match Buyer Reality

There’s a saying that’s especially important in today’s market, and it’s: “if your price isn’t compelling, it’s not selling.” Maybe that’s what happened with your house.

With mortgage rates where they are and inflation driving up the cost of everyday purchases, buyers have less room to stretch. If they feel like your house is priced even a little high, it’s going to get skipped over. And if no one looks at it, it’s not going to sell.

The Fix: Price to draw buyers in, not push them away. Have an agent pull fresh data from recent sales so your asking price matches what buyers are actually paying right now.

2. The First Impression Didn’t Win the Click

Most buyers decide whether they want to tour a home in seconds. If the photos look dark, or dated, they scroll right past. And while you may think: “If they just saw it in person, they’d get it,” you may not get that chance.

And honestly, even in person, small things can quietly kill momentum – worn down paint, outdated fixtures, clutter, or a yard that feels high-maintenance. Individually, they’re small. Stacked together, they create doubt.

The Fix: Walk the house like you’re a buyer, not the owner. Start with what’s easy and obvious – paint, lighting, curb appeal, decluttering. Then update the photos so they match the best version of your house.

3. The Marketing Was Too “Set It and Forget It”

Today, the number of homes for sale has grown in many areas. Buyers have more options, which means your house needs a plan to stand out. A generic description and a basic upload to the MLS can blend in fast.

The Fix: Find an agent who can build stronger exposure through digital marketing and social platforms, plus content that makes buyers stop – strong photos, a smart description, a video walk-through, and a plan for open houses and follow-up.

4. There Was No Clear Plan for Feedback

Sometimes the house gets showings, but no offers. If that was your experience, it actually tells you something important. Buyers liked it enough online to come see it. So, something else was holding them back.

Those buyers were sending a message. It just wasn’t translated into action.

The Fix: Make sure your agent has a clear plan for seeking out and acting on feedback quickly. That dialogue often points to the one change that would get a house sold.

5. The Deal Couldn’t Get Over the Finish Line

Even when a house is priced well and marketed right, deals fall apart when there’s no plan for the human side of the transaction.

Buyers today are more likely to ask for repairs, credits, or help with closing costs than a few years ago. In this type of market, being unwilling to negotiate can cost you more than a reasonable concession ever would.

The Fix: Decide ahead of time what matters most to you and where you can be flexible. Keep the dialogue open and lean on your agent for advice.

Bottom Line

If your house didn’t sell the first time, you’re not stuck. You just need a different strategy, and maybe a different partner.

When you’re ready for a fresh set of eyes on what happened and what to change first, let’s connect.