Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Fresh Inspiration for Spaces You Love

Color trends aren’t just about what looks beautiful — they reflect how we want to live and feel in our homes. Each year, leading color authorities reveal shades that capture the cultural moment, and 2026 is all about warmth, depth, comfort, and calm clarity.

Whether you’re refreshing a single room or preparing your home for the market, these standout selections from the industry’s biggest names offer timeless inspiration.

🖌️ Benjamin Moore — Silhouette AF-655

Bold yet refined, Silhouette AF-655 is a dramatic espresso brown with soft charcoal undertones. This rich hue brings depth and sophistication to a space without feeling heavy or overwhelming.

Think cozy libraries, elegant dining rooms, statement-making built-ins, or a moody accent wall that instantly elevates a room. Silhouette creates a sense of intimacy and luxury — perfect for homeowners craving warmth and character.

Why it works in 2026:

We’re seeing a continued shift toward grounded, earthy tones that make homes feel secure and welcoming. Silhouette embraces that mood beautifully.

🏡 Sherwin-Williams — Universal Khaki (SW 6150)

Universal Khaki is the definition of a modern neutral. Warm, earthy, and incredibly versatile, it bridges traditional and contemporary design styles effortlessly.

This shade works beautifully in living rooms, kitchens, and open-concept spaces where you want a cohesive, comforting backdrop. It pairs well with crisp whites, soft blues, rich greens, and even bold accent colors.

Why it works in 2026:

Buyers and homeowners alike are gravitating toward timeless palettes. Universal Khaki provides flexibility — making it easy to layer textures, décor, and personal style without committing to something trendy or fleeting.

☁️ Pantone — Cloud Dancer (PANTONE 11-4201)

In a refreshing move, Pantone selected a white-based hue for 2026. Cloud Dancer is soft, clean, and calming — evoking clarity, renewal, and a fresh start.

Unlike stark whites, this shade has subtle warmth that makes it feel approachable. It reflects light beautifully and pairs seamlessly with nearly every color in the spectrum.

Why it works in 2026:

After years of bold statements and saturated tones, many homeowners are craving simplicity. Cloud Dancer offers breathing room — the perfect canvas for layered textures, natural materials, and personal touches.

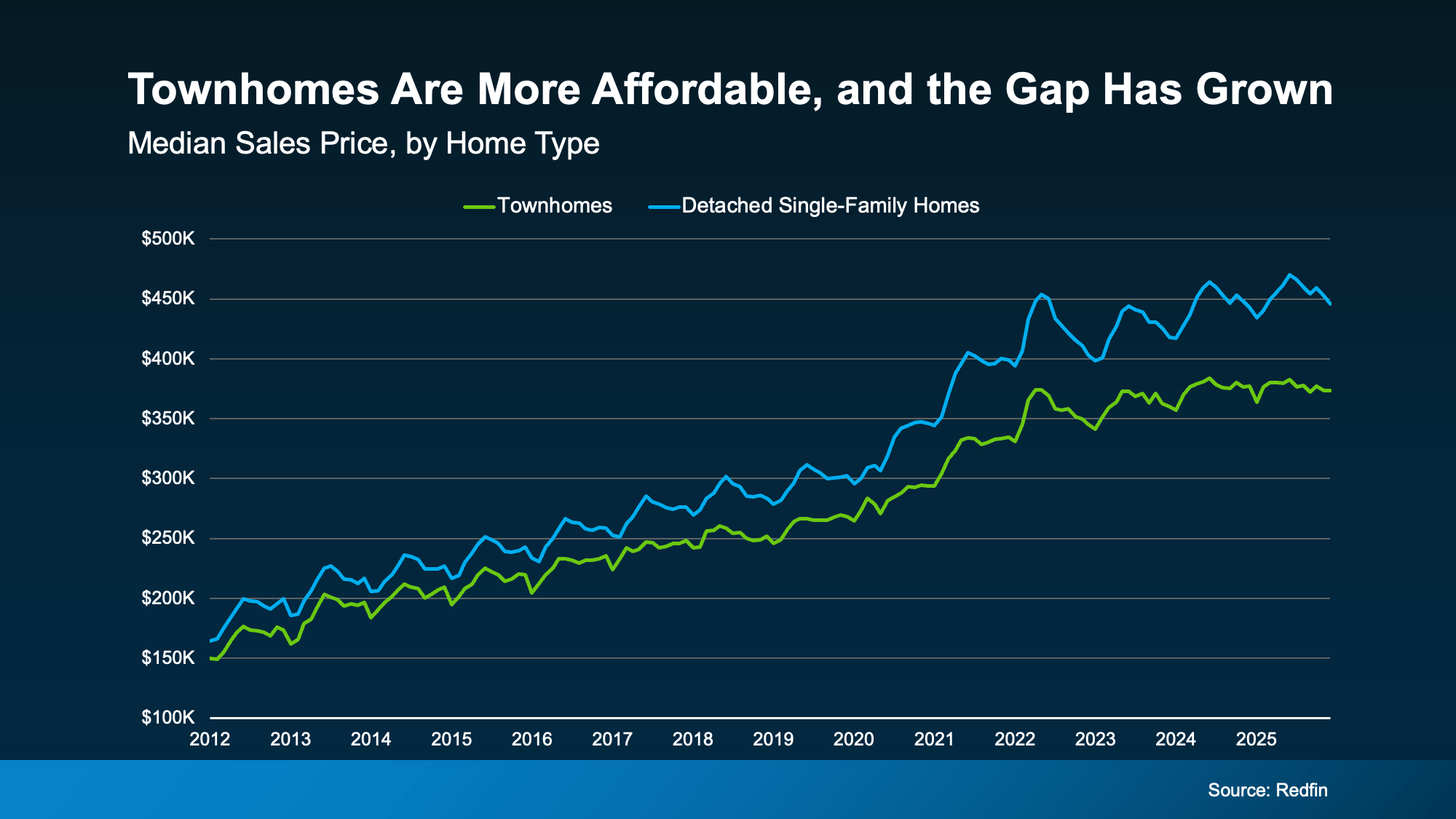

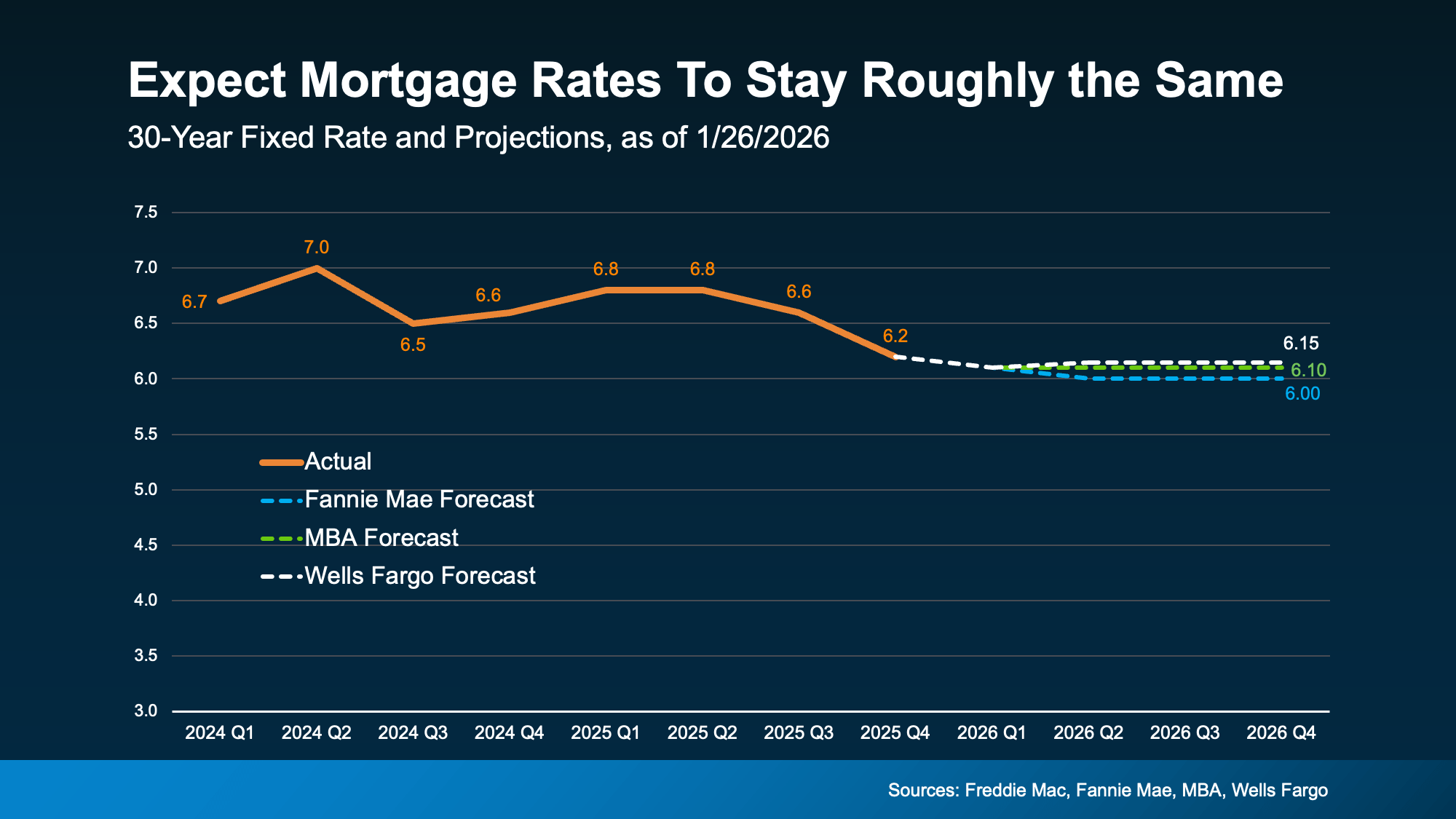

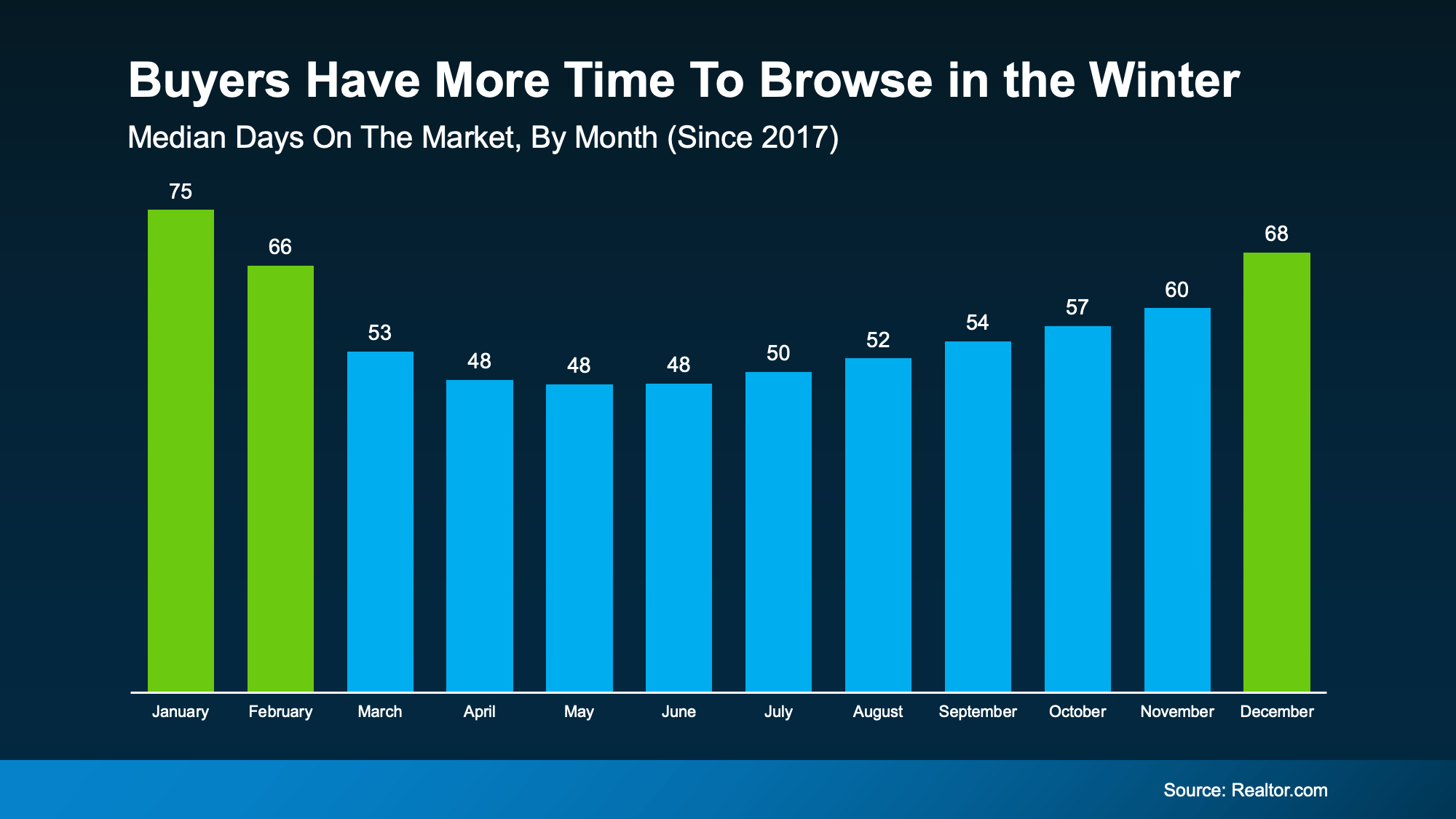

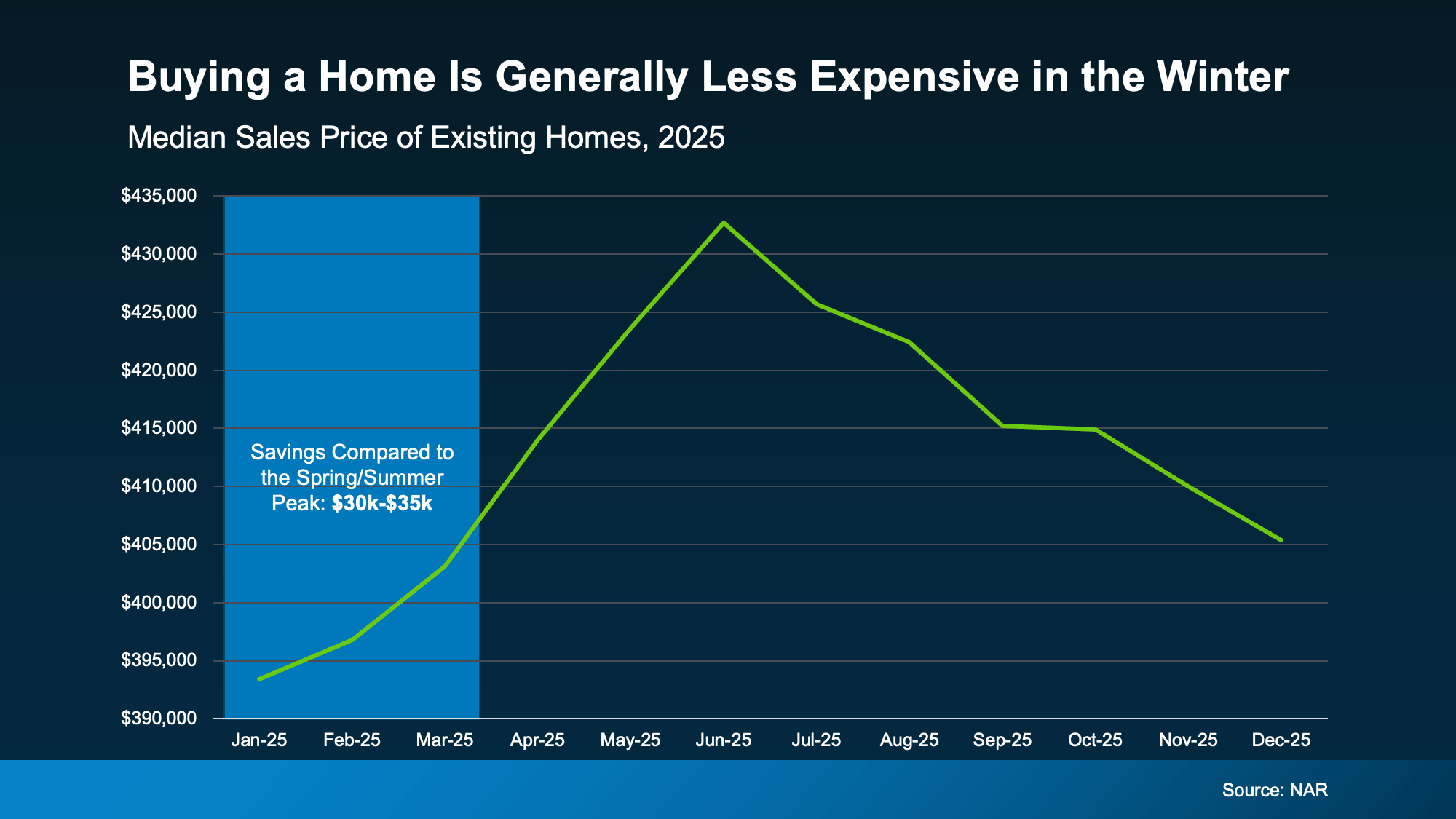

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

So, What Can You Do About It?

So, What Can You Do About It?