Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

There’s a lot of noise out there right now about investors in the housing market.

Some headlines make it sound like big Wall Street firms are buying up everything in sight. And if you’re trying to purchase a home yourself, that can make it feel like the odds are stacked against you.

But when you take a closer look at the data, a very different picture starts to come into focus.

Most Investors Are Just Everyday Owners

For starters, when you hear the word investor, you probably picture big corporations. And that misconception is a large part of what’s feeding into the myth that they’re buying up all the homes.

Most investors aren’t big companies, at all.

They’re everyday people just like you.

They’re someone who owns a second home (like a vacation house at the river), a neighbor who has 1 or 2 rentals, or even a homeowner who tried to sell their home, didn’t get the price they wanted, and decided to rent it instead.

And when all of these groups are lumped together in the headlines, the number of investors sounds high – especially if you’re operating under the assumption all investors are big investors.

But here’s what the numbers really show when you drill down.

Institutional Investors Are a Small Slice of the Housing Market

Large institutional investors, those big companies buying homes, actually make up a very small share of the overall housing market.

According to BatchData, the largest investors (those with 1,000+ homes) own just 0.4% of the 86 million single-family homes in the country. And their share of the market is actually shrinking.

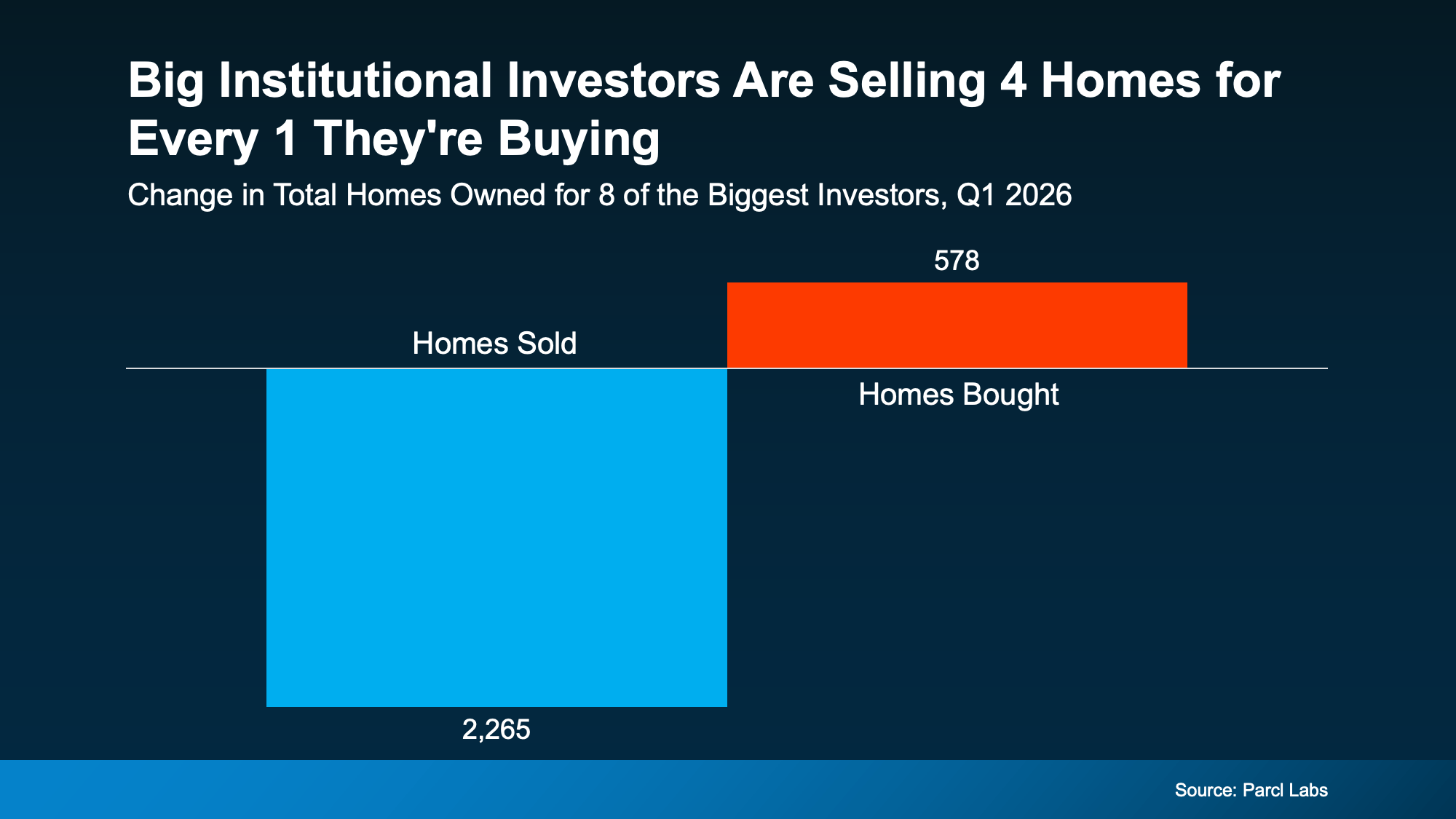

Data from Parcl Labs shows big investors are selling 4 homes for every 1 they’re buying right now (see visual below):

That means they’ve actually added almost 1.7k homes back into the market lately.

That means they’ve actually added almost 1.7k homes back into the market lately.

What This Means for You

The story is clear. Instead of aggressively buying up homes, most of these companies are stepping back, which means less competition from them than you might expect. If you were someone who thought they were dominating the market, let that give you some peace of mind.

Most of the competition you’ll face is from other everyday buyers – people just like you. And with most large investors stepping back, there may be more opportunity in the market than you think.

Bottom Line

It’s easy to assume big investors are taking over the housing market, but the data tells a different story. If you want an expert’s opinion on what investor activity looks like in our area, let’s talk.

Because odds are, it’s not as big a factor as you may think.

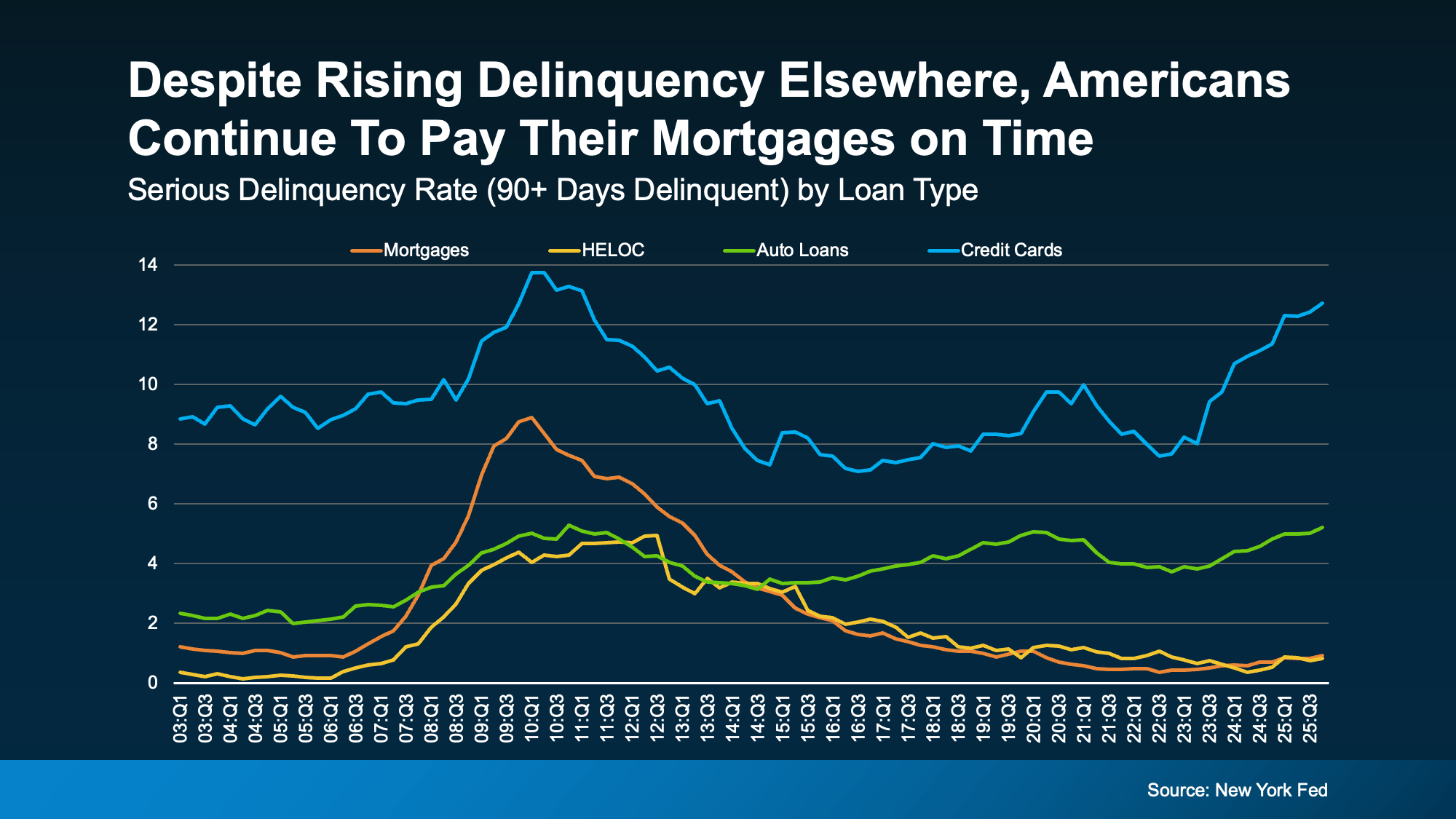

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

In other words, people may fall behind on other debts, but they fight hard to keep their homes. And, in today’s housing market, they’re also in a strong equity position to do so.

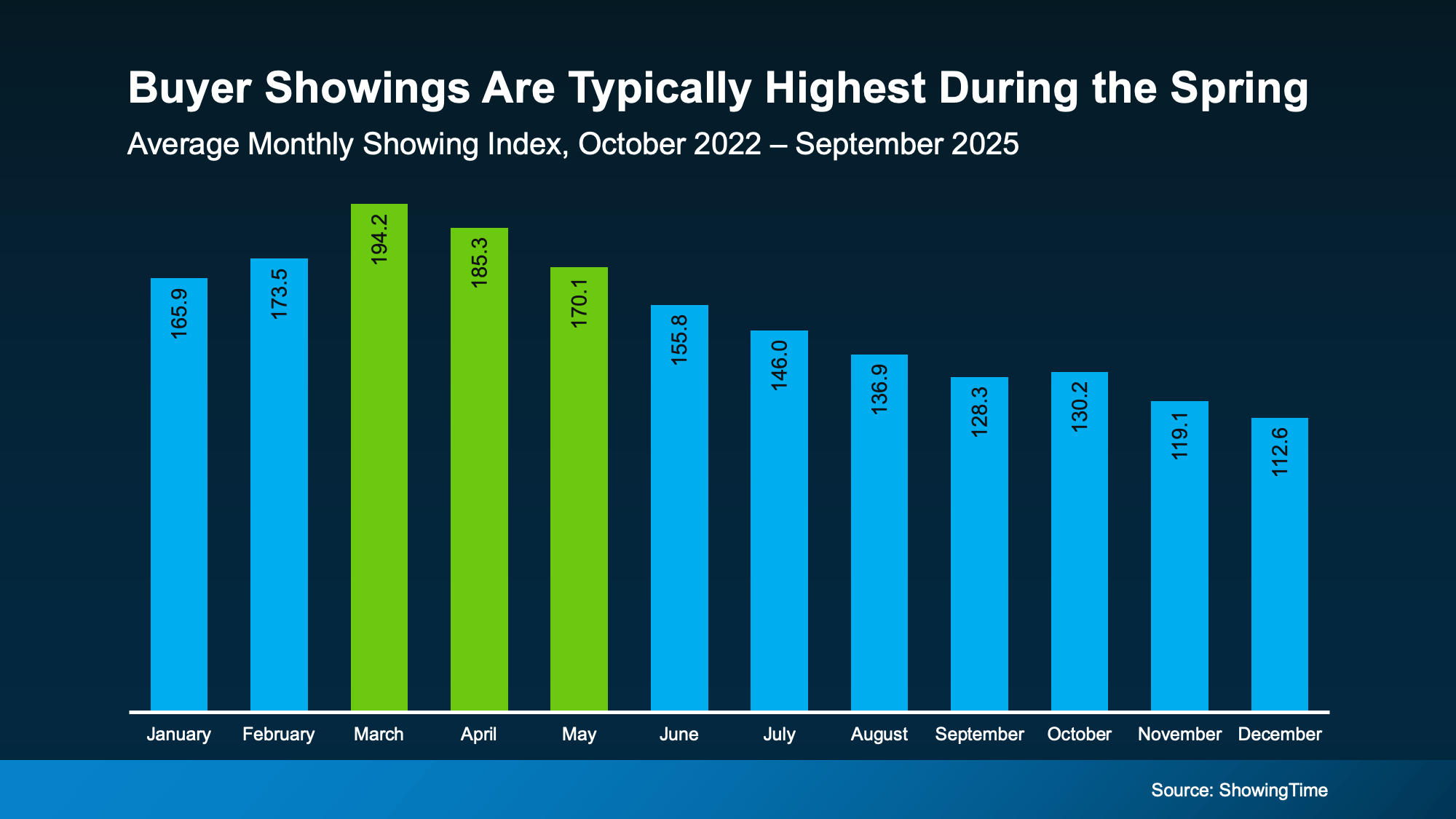

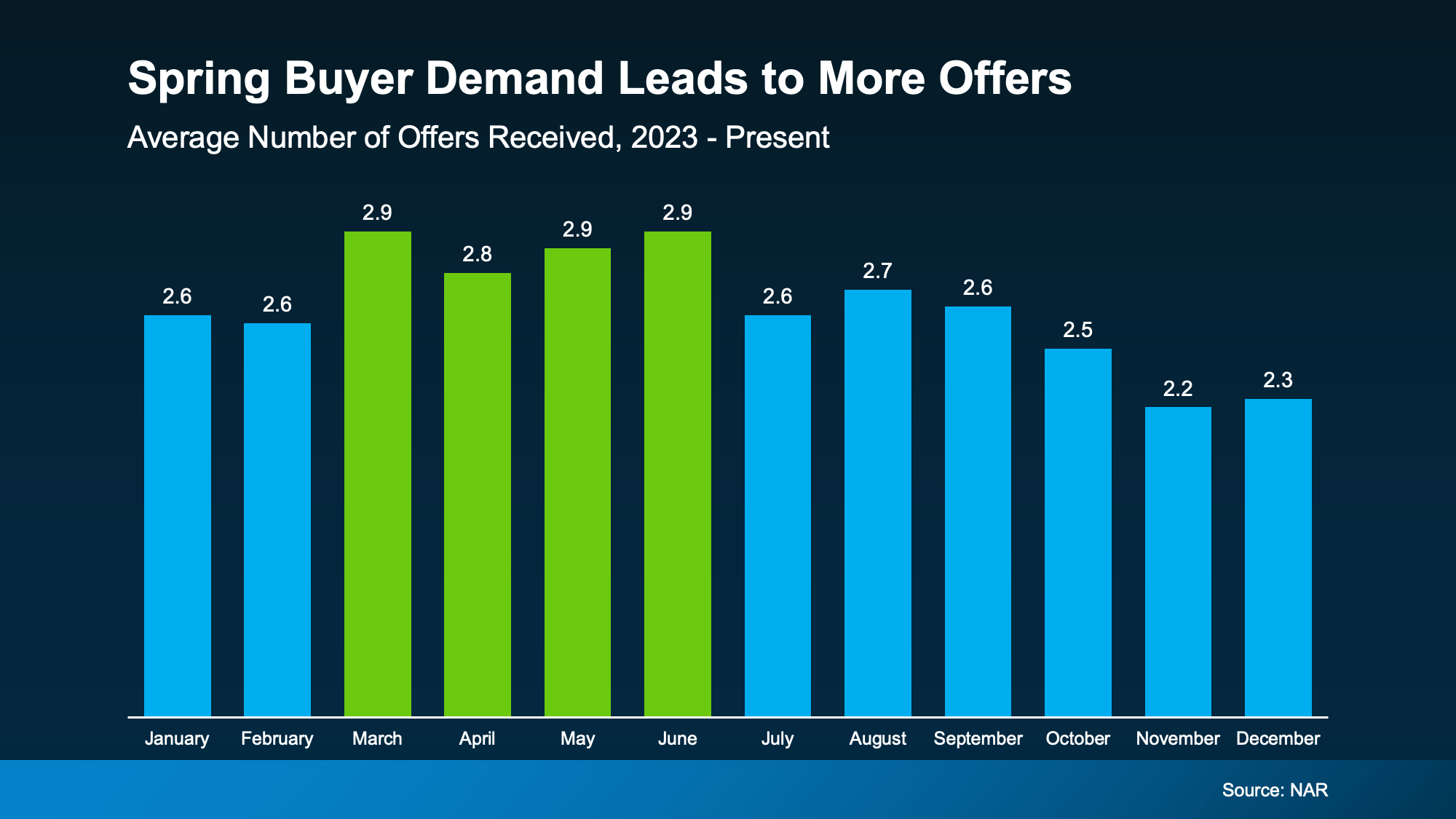

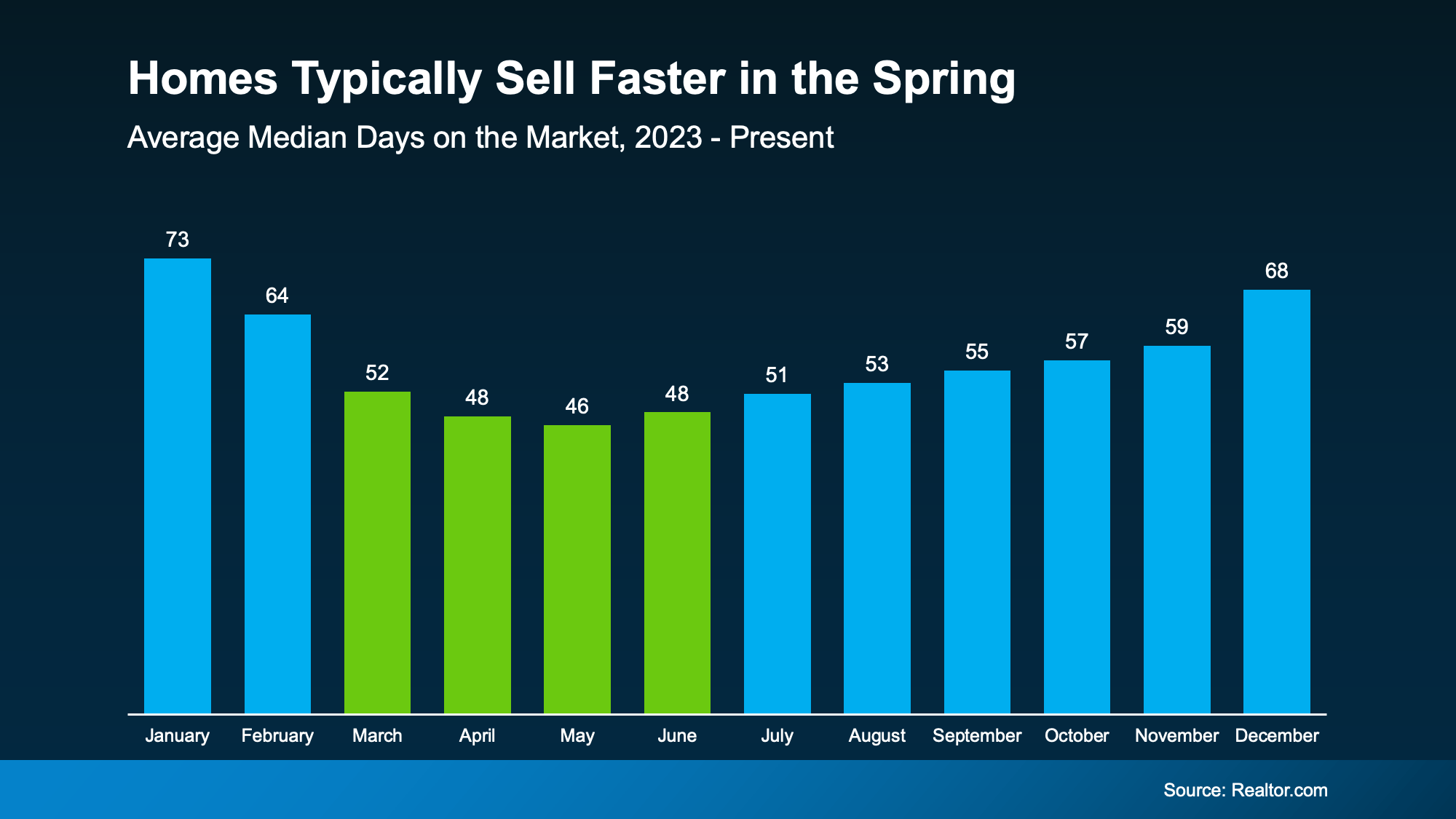

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that’s a difference you can feel.

On average, homes sell 20 days faster in the Spring compared to the Winter. That’s almost 3 weeks shaved off your timeline. And that’s a difference you can feel.