Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

There’s a lot of uncertainty right now and that’s leading to some dramatic headlines. And if you’re thinking about buying a home, that can make you feel a little less sure about your decision.

A recent study by CNBC asked homebuyers what they’re most worried about, and three themes kept coming up again and again:

- Mortgage rates

- The number of homes for sale

- Home prices

But a lot of what you may be hearing on those is based more on misconceptions. Not facts. So, let’s break it down and separate fact from fiction.

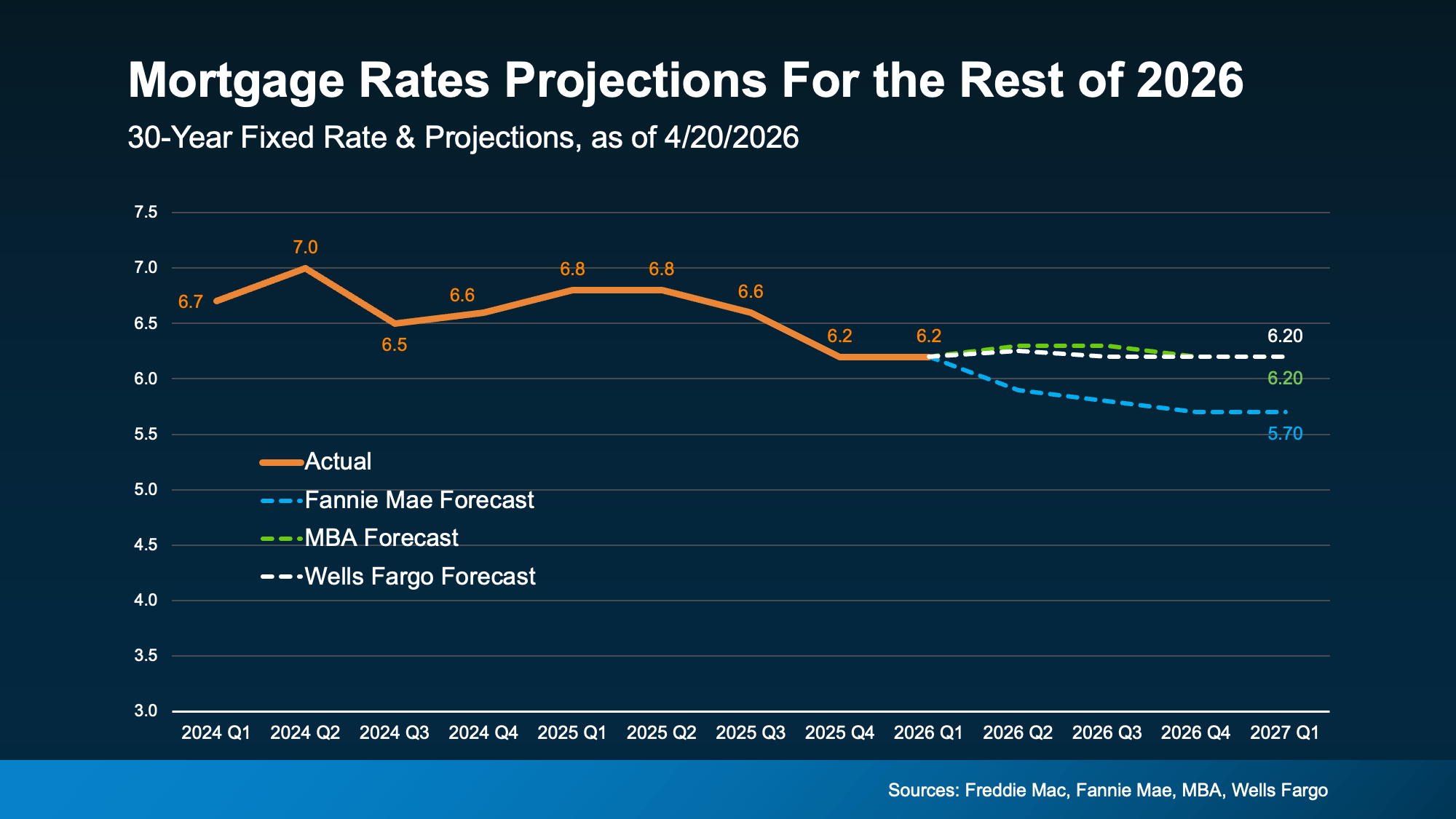

Misconception #1: “I’ll Just Wait, Because Mortgage Rates Are Going To Fall Dramatically”

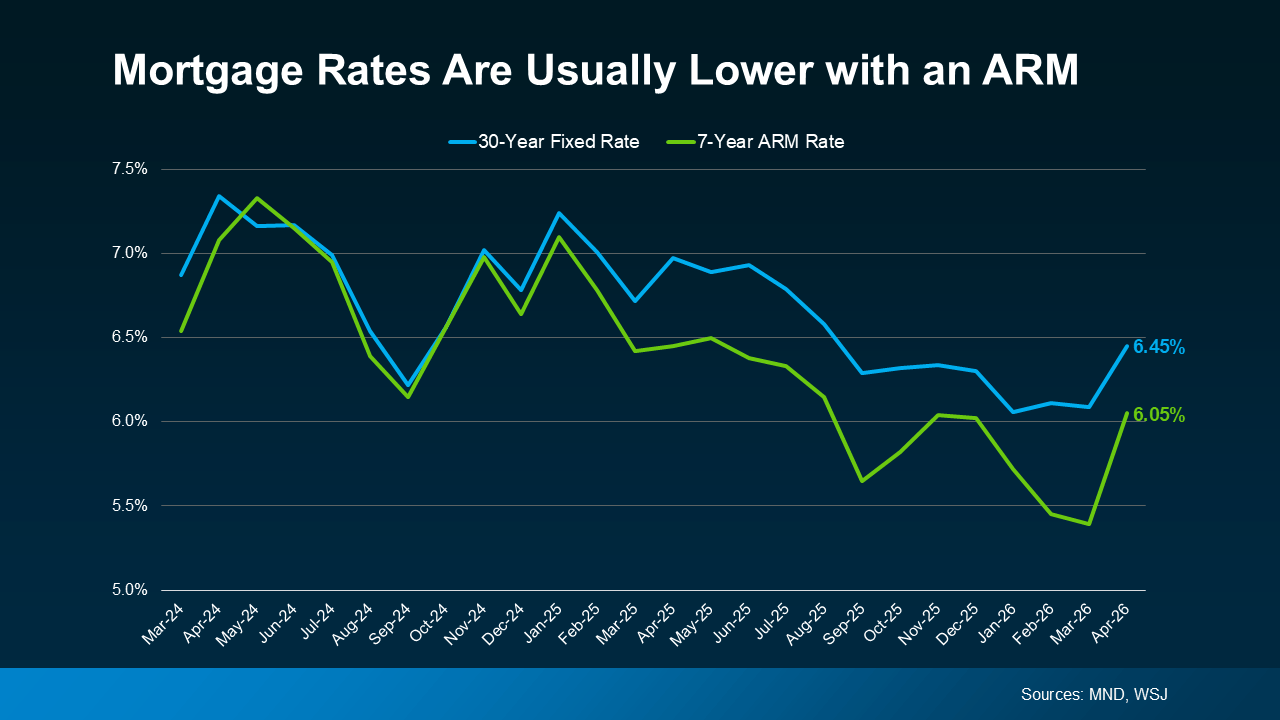

One idea doing its rounds on social is that mortgage rates are going to drop dramatically soon. So, it’s better to wait to buy.

But is that really what’s expected?

While mortgage rates have come down a bit in the last few weeks, forecasts don’t show a major drop ahead. The most likely scenario is that rates stay somewhere in the low 6% range this year.

And that’s not a big change from where rates are now (see graph below):

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

Of course, this depends on where inflation and the economy go from here. But, based on what we know today, waiting for a big drop in rates may not work out the way some people hope. As U.S. News explains:

“Mortgage rates aren’t expected to change much over the next several quarters . . .”

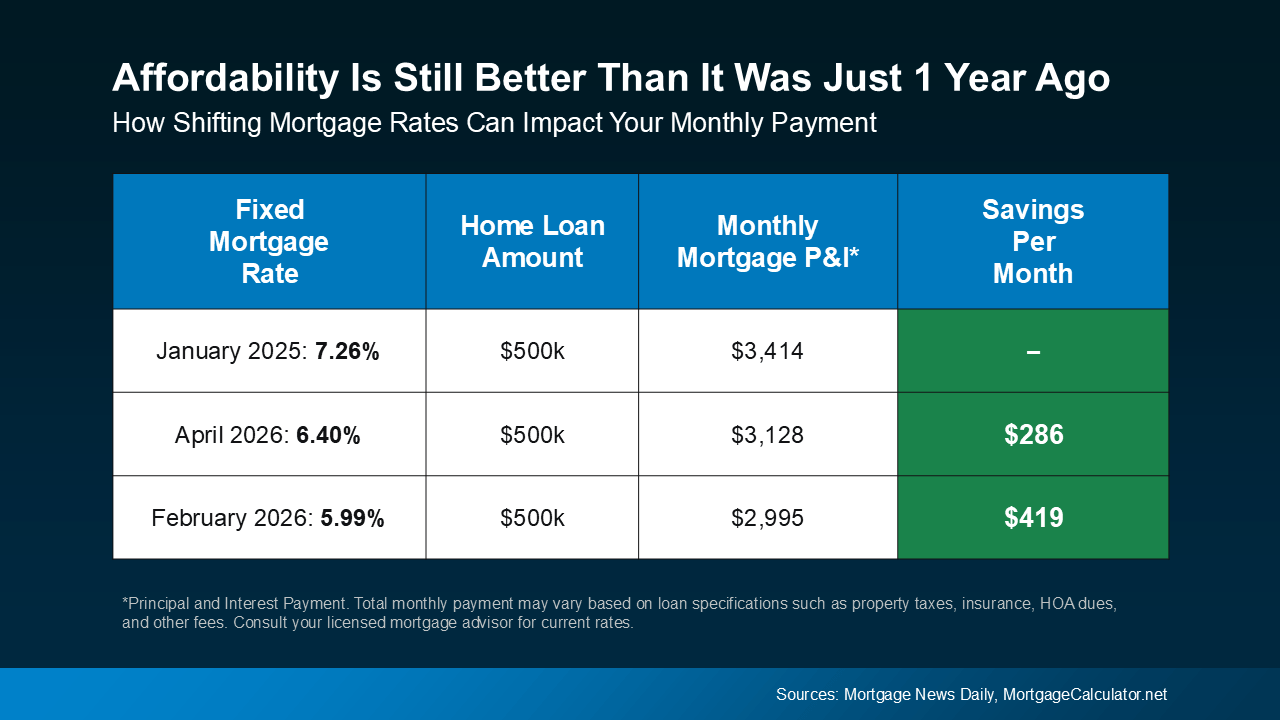

Not to mention, even with rates where they are today, it’s already more affordable than a year ago. So, even if they don’t change much, it’s still better than it was.

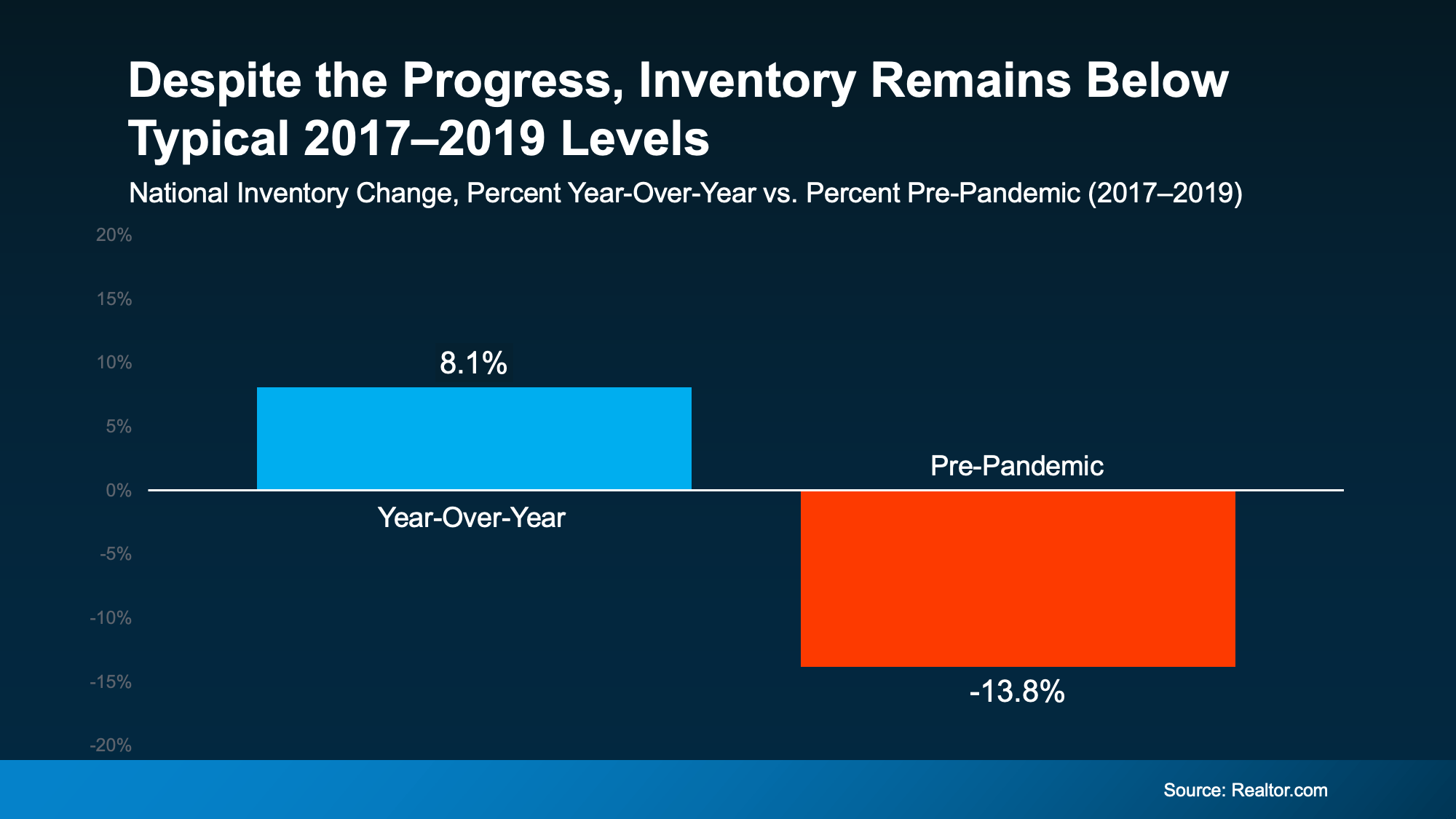

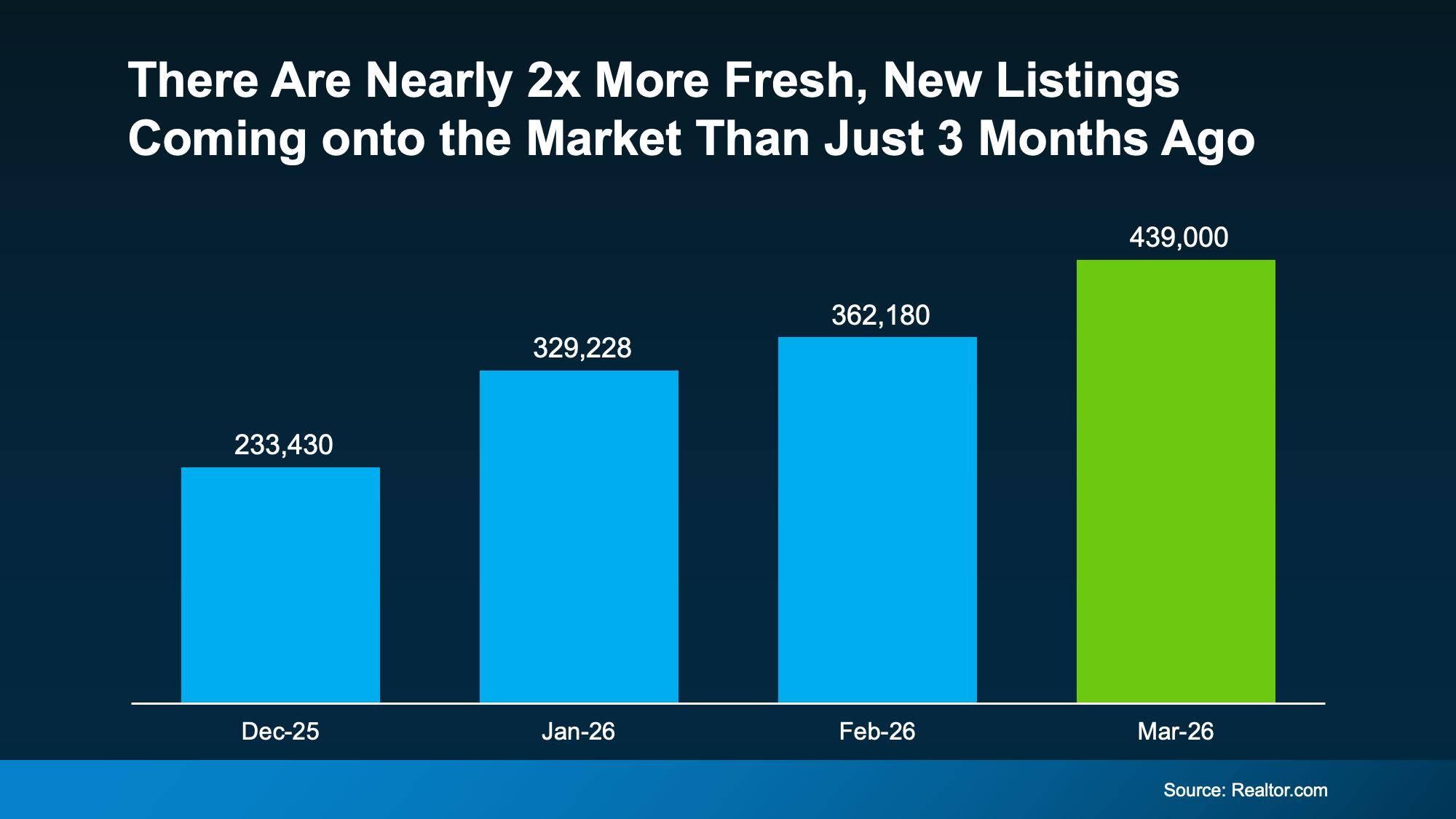

Misconception #2: “There Are Too Many Homes for Sale Right Now”

You’ve probably heard inventory is up. And nationally, it is. The number of homes for sale is 8% higher than this time last year. But that’s not a bad thing. In fact, it’s one of the reasons buyers have a bit more breathing room right now.

The problem is the headlines are making something good, sound bad. They’re focusing on how this is the most inventory we’ve had since 2019 or how many homes builders are building. And that can make it sound like the number of homes for sale is rising too far, too fast.

But that’s not what the bigger picture shows.

Data from Realtor.com proves that, even though inventory is up compared to last year, it’s still nearly 14% lower than it was during the last normal housing market (2017-2019):

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

While it can vary a lot based on where you live, only 9 states have more inventory than pre-pandemic today. That’s a key reason why there still aren’t enough homes for sale to trigger something like the crash back in 2008.

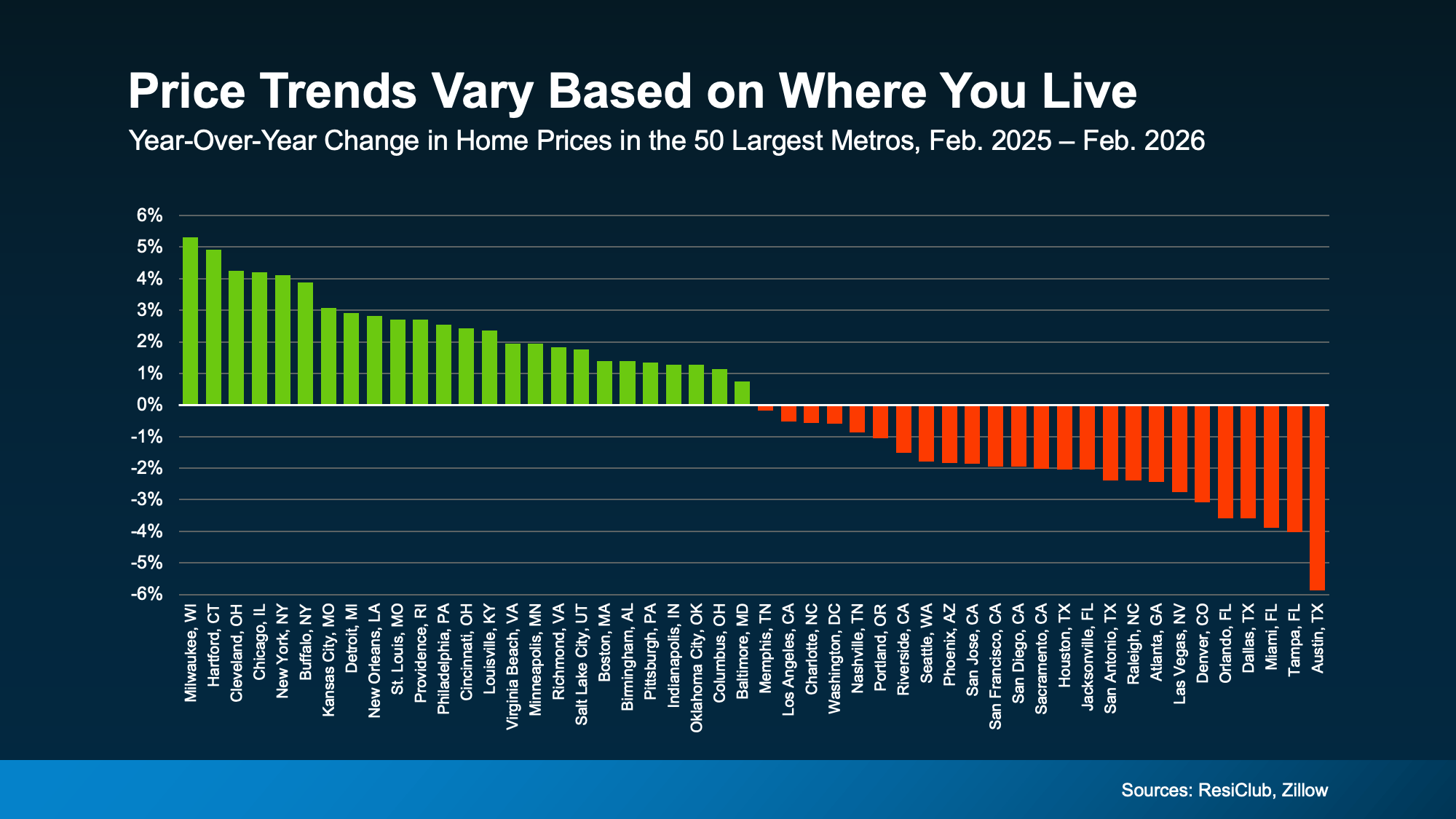

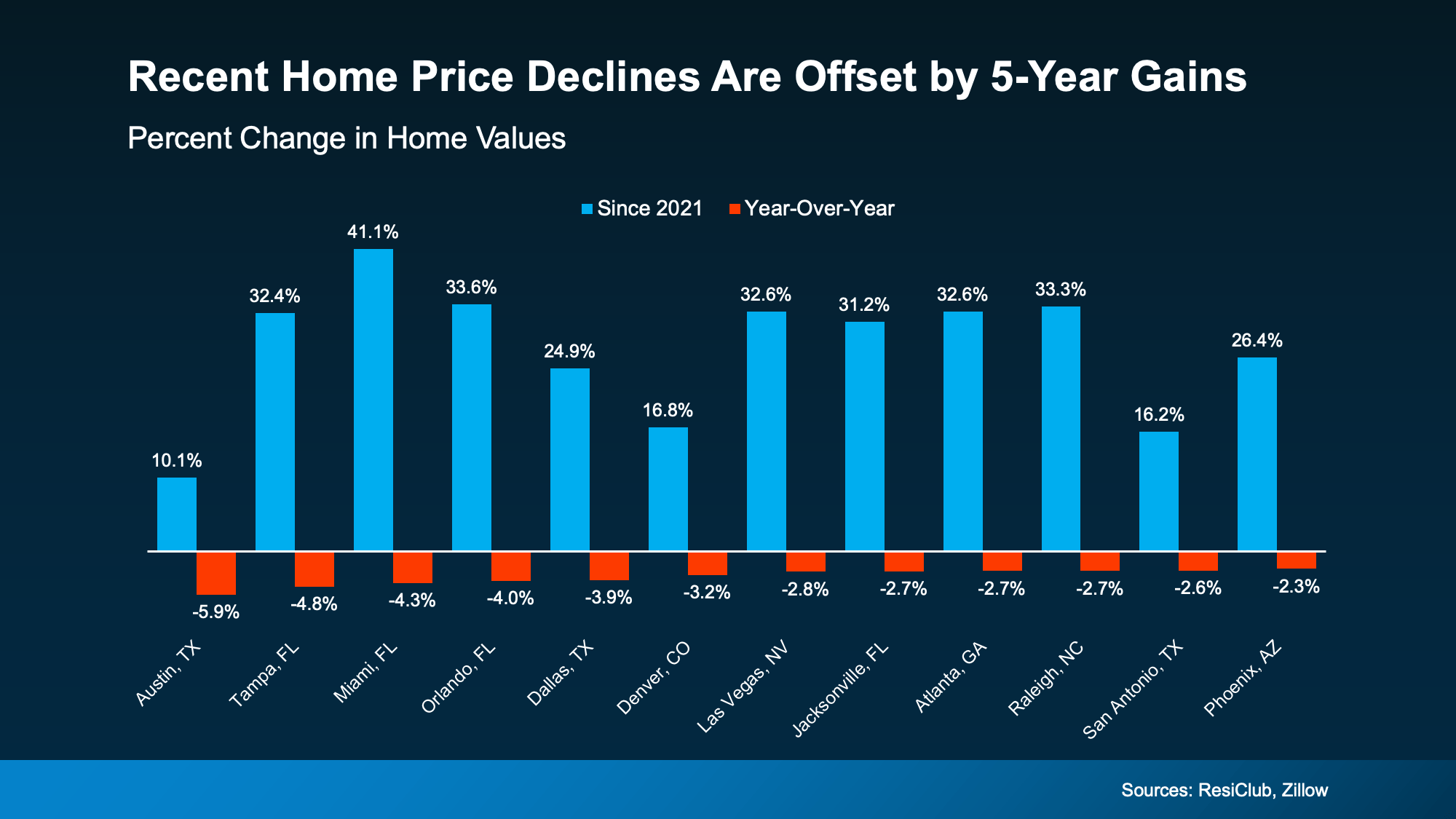

Misconception #3: “Home Prices Are About To Crash”

You’ve probably seen this one, too. The confusion is coming from the fact that some metros are experiencing slight price declines. And influencers are running with that and saying prices are crashing. But that’s not the reality.

Most areas are seeing prices rise, not fall. And that’s because:

- Many homeowners aren’t selling because they don’t want to give up the low mortgage rate they locked in a few years ago. And that’s keeping a lid on how much inventory can grow.

- Since inventory is still below pre-pandemic norms, there aren’t enough homes for sale to cause a price crash.

- And even in markets with more inventory, some sellers are choosing to pull their homes off the market instead of cutting prices.

And those are 3 big reasons prices aren’t headed for a crash.

And even in the markets experiencing mild declines, the drops aren’t enough to cancel out the big gains most homeowners have seen in the last 5 years (see graph below):

That’s not a crash. That’s just prices moderating after a few record-breaking years.

That’s not a crash. That’s just prices moderating after a few record-breaking years.

Bottom Line

Online posts are going to make things sound worse than they are. If you want a true, data-bound look at what’s really happening in today’s market, lean on a real estate agent.

Let’s connect so you have someone to separate fact from fiction today.

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

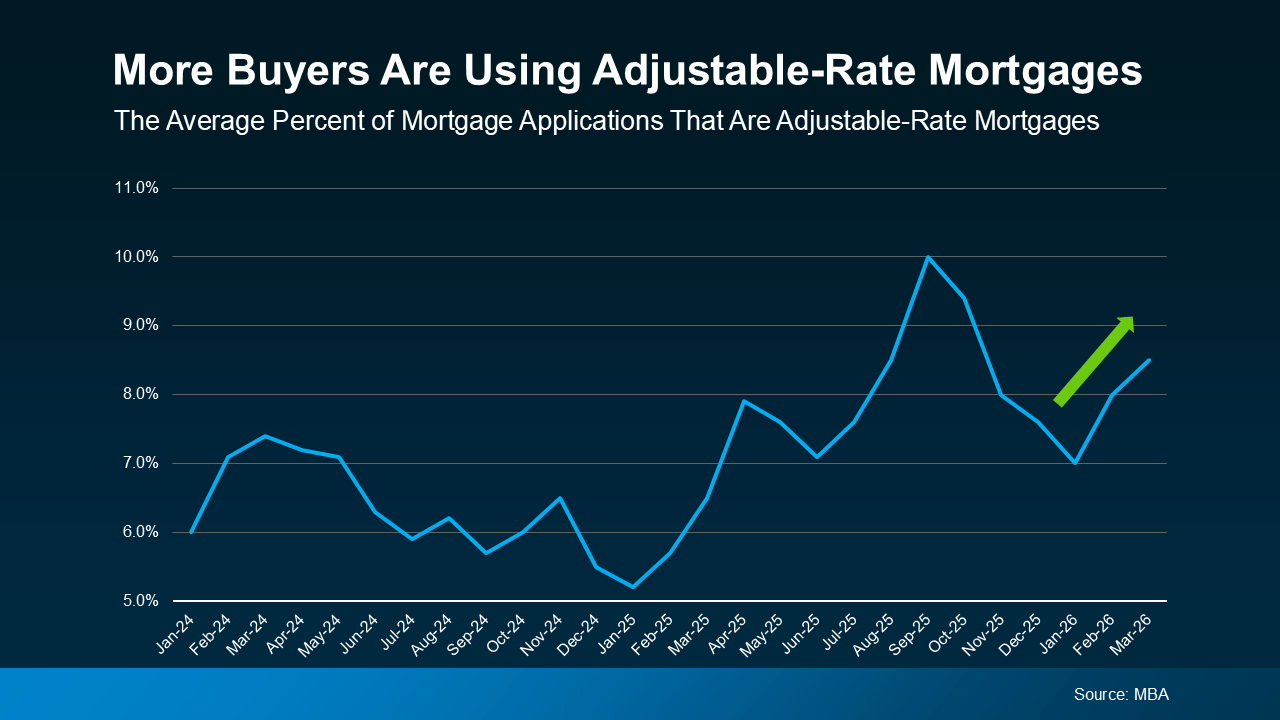

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage. And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.